Source – theguardian.com

- ‘…As I keep stating, the Great Crisis… the one to which 2008 was a warm-up, has finally arrived. In 2008 entire banks went bust. In 2022, entire countries will do so”

What Happens to Stocks When the 5th Largest Economy in the World Goes Bust?

By Graham Summers, MBA

(Also Read: Liz Truss resigns, U.K. markets in turmoil: What’s behind the crisis and what you need to know @ https://www.theglobeandmail.com/world/article-liz-truss-resignation-british-economy/)

One of the central theses of my bestselling book The Everything Bubble is that once a central bank embarks on a path of extraordinary monetary easing, it can never escape.

(Also Read: Economy in crisis, Tories in meltdown: how I have told the sad, strange story of Britain @ https://www.theguardian.com/commentisfree/2022/oct/17/economy-crisis-tories-britain-brexit-johnson-truss-us)

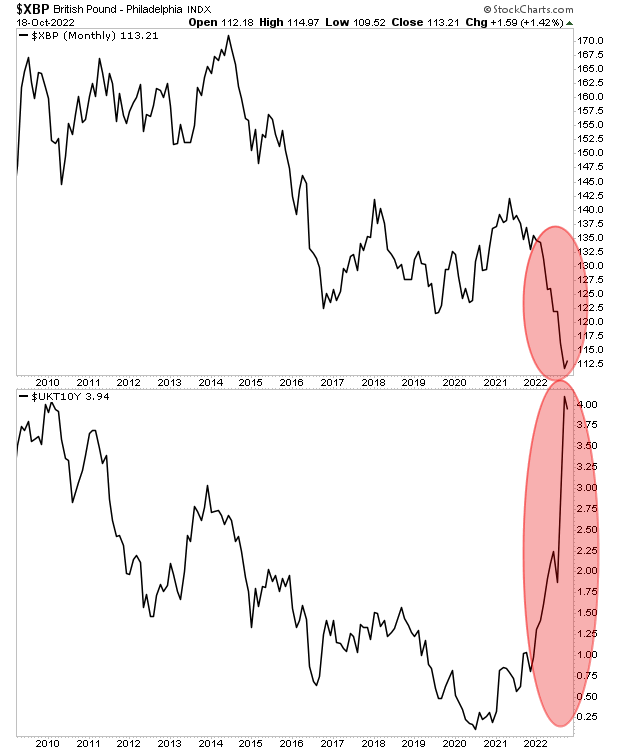

The Bank of England (BoE) is now finding this out the hard way. Back in September it had planned on shrinking its balance sheet via a process called Quantitative Tightening (QT).

Then the new government introduced more fiscal easing, the British Pound collapsed and the yields on British Government bonds exploded higher.

The BoE was forced to abandon all plans on QT and instead introduced emergency, unlimited Quantitative Easing (QE) to try and calm the markets.

The new plan was to provide QE for a few weeks until things calmed down. In fact, this “temporary” QE was supposed to end October 14. However, the BoE was forced to provide additional easing measures to make sure things remain calm.

So QE is ending… but easing is not. And the BoE claims it will once again try to start QT on November 1st.

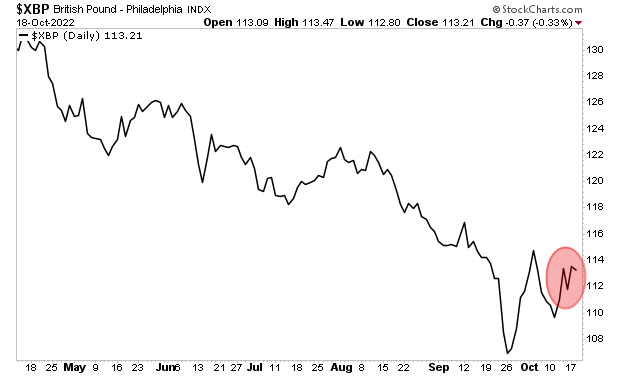

Good luck with that! The Pound is already rolling over again!

As I keep stating, the Great Crisis… the one to which 2008 was a warm-up, has finally arrived. In 2008 entire banks went bust. In 2022, entire countries will do so.

The U.K. is the fifth largest economy in the world. And by the look of things, it will be the first to go bust. It won’t be the last. Japan, Europe and ultimate the U.S. will experience debt crises in the coming months.

Smart investors are preparing for what’s coming now… before it arrives

Related…

Economy in crisis, Tories in meltdown: how I have told the sad, strange story of Britain

Brexit, Johnson, Truss’s U-turns – I have tried to explain it all to a US audience. I’ve found it hard to take it all in myself

- Stryker McGuire is a former editor at Newsweek and Bloomberg

Illustration by Matt Kenyon

Since the 1990s I’ve been interpreting events in Britain for an American audience through my journalism. Sometimes it’s easy: London’s glorious renaissance, Tony Blair’s rise. Sometimes it’s less easy: the strangeness of a “special relationship” where one side cares too much and the other too little, the post-imperial hangover that courses through British life.

And sometimes it’s hard: the puzzle of Brexit, the precipitous downfall of the Conservative party. It helps that for Americans still living through the Donald Trump saga, nothing is outside the realm of possibility any more. It also helps when I explain to them that those two latest chapters of British history are connected.

I tell them that from the 2016 referendum onward, Brexit increasingly gave the Tories a focus. Never mind that Brexit was the most divisive event in postwar Britain; over time, the struggle to make it happen unified the party. Boris Johnson’s “Get Brexit Done” 2019 election campaign cemented the transformation and, as far as Brexit went, silenced Labour.

Within six weeks, however, the Tory tide would turn. Once Britain formally left the EU, the Brexit-imposed discipline within the Conservative party began to unravel. Admittedly, the pandemic would have thrown any government off course, but Johnson’s conduct in office didn’t help the Tory brand or party unity. Swamped by scandal, he was out. Enter Liz Truss.

As the US and the world looked on, Truss’s first weeks in office did not exactly restore confidence in Downing Street. Suddenly, the new government was shredding the Tories’ reputation for fiscal prudence and sound economic management. Friends of mine in the States could barely believe what they were witnessing. Even Americans who are ideologically opposed to the Conservatives were shocked to see the party of Churchill and Thatcher flying off the rails.

Liz Truss speaks after the sacking of Kwasi Kwarteng as chancellor, 14 October 2022. Photograph: Daniel Leal/AFP/Getty Images

The Truss-Kwasi Kwarteng “Growth Plan 2022” started out as a budget at war with itself, with vast emergency spending sitting alongside big unfunded tax cuts. It was also at war with Bank of England monetary policy. That was bad enough. Then came U-turns, the defenestration of Kwarteng and the naming of a new chancellor, Jeremy Hunt, hardly an ideological soulmate of the libertarian prime minister.

This story is far from over. From the outset, the reaction to the new government’s “fiscal event” abroad was awful. Former US Treasury secretary Larry Summers said the world’s fifth-largest economy was “behaving a bit like an emerging market”. President Biden himself said that Truss’s original plan was a “mistake”. The International Monetary Fund, which usually reserves its sermonising for developing economies, said: “we do not recommend large and untargeted fiscal packages at this juncture, as it is important that fiscal policy does not work at cross purposes to monetary policy. Furthermore, the nature of the UK measures will likely increase inequality.”

Still, with all the opprobrium heaped on Truss, it’s easy to forget that the damage began long before she got hold of Britain’s finances. What’s happening today cannot be separated from what happened in the last decade, leading up to Brexit. To explain those days to non-Britons, you have to wade into the weeds of British politics. There, we come upon Nigel Farage, who though never elected to parliament had an extraordinary influence on Westminster politics. Had it not been for the threat Farage and Ukip posed to the Conservative party, David Cameron may never have decided to call for a referendum. But, fatefully, he did.

As a dual US-UK citizen who’s lived in London since 1996, the closest I could get to understanding a rationale behind Brexit was to see it in the context of what Blair once called “post-empire malaise” – a vague if deep-seated yearning to regain the confidence and sureness of identity that, at least in the imagination, went hand in hand with running an empire. “Take back control” was surely part of that, fuelled also by heightened economic insecurity in the wake of the 2007-08 financial crisis and a concomitant unease about immigration.

Setting that logic aside, I have to say that virtually all the economic arguments in favour of Brexit looked specious at best and cynically misleading at worst. In that sense, Brexit is a kind of original sin that sits at the heart of today’s UK economy. That should have been evident in the myriad dire economic forecasts blithely dismissed as “remoaner” scaremongering in the run-up to the 2016 referendum – forecasts that turned out to be mostly accurate. And it should have been obvious– as it was to the rest of the world – in the downward trajectory of the “Brexit pound”, which fell from 1.50 to 1.33 to the dollar overnight after the 23 June 2016 vote and ultimately hit its lowest-ever recorded level of 1.03 on 26 September of this year.

Being “liberated” from the EU was never going to live up to the counterfeit promises made by the Vote Leave campaign before the referendum. Britain’s borders are no less porous than they were. The post-Brexit trade deals the UK has negotiated are insignificant compared with the loss of its largest trading partner. The jewel-in-the-crown deal with the US is not even on the agenda, as Truss admitted last month.

The pandemic, whose arrival coincided with Britain’s departure from Europe, camouflaged much of the toll Brexit was inflicting on the economy. But the harm is real. A year ago, the Office for Budget Responsibility was estimating that Brexit’s long-term impact on economic growth would be more than twice as damaging as that of Covid.

The effect on trade has been devastating. Modelling by the Centre for European Reform found that solely because of Brexit, British trade in goods was down during the first half of last year, ranging between 11 and 16% month to month. “There is evidence that businesses face new and significant real-world challenges in trading with the EU that cannot be attributed to the pandemic,” the House of Lords European affairs committee reported in December.

Ending the free movement of labour between Britain and the continent – a Brexit cornerstone – is hollowing out the workforce. According to the Office for National Statistics, the number of job vacancies stood at 1,246,000 in the third quarter of this year, up from about 823,000 before Brexit and Covid-19 set in. These shortages afflict businesses large and small, from cafes and pubs to farms and manufacturing plants.

Meanwhile, the OBR analysis from May shows a number of economic indicators all going in the wrong direction: as a result of leaving the EU, long-term productivity will slump by 4%, both exports and imports will be around 15% lower in the long run, newly signed trade deals with non-EU countries “will not have a material impact”, and the government’s new post-Brexit migration regime will reduce net inward migration at a time of critical labour shortages. It has been some story to tell.

There’s a scene in the House Commons that keeps playing in my head. It’s 2019 and Jacob Rees-Mogg, now Truss’s business secretary, is speaking of the “broad, sunlit uplands that await us” thanks to Brexit. Then I contemplate where Britain is today: heading into a protracted recession under an enfeebled prime minister leading a wounded, fractious party. I hope I’m proved wrong, and those sunlit uplands are out there over the horizon. No sign as yet. But I’d be pleased to come back and tell everyone who has listened so far that I was mistaken.

- Stryker McGuire, who lives in London, is a former editor at Newsweek and Bloomberg