Source – zerohedge.com

– “…The development of crypto currencies is perhaps the biggest libertarian movement we have seen in history. It is nothing short of a revolution led by a group of individuals fostering similar political ideologies. In some ways, cryptos could be seen as attempts to form new governments if not just central banks”

Pipe Dreams And Ponzi Schemes

Crescat Capital’s commentary for the month ended December 2021, titled, “Pipe Dreams and Ponzi Schemes.” [munger]

Q3 2021 hedge fund letters, conferences and more

Normally, as part of the creative destruction process in economic downturns, the financial system gets purged of excesses. In the subsequent recovery, the health of the economy is restored in a natural way as new leadership arises from sectors and industries that are inherently different from those of the prior expansion. In the wake of some of the biggest profligacies, the disorderly unwinding of pipe dreams and Ponzi schemes coincides with the economic contraction and results in the permanent loss of capital for those caught up in them. As Warren Buffett says, “Only when the tide goes out, do you discover who’s been swimming naked”. A universal problem with every business cycle as it advances to its later stage is that investors tend to extrapolate recent success of strong performing industries and asset types driving further momentum and speculative frenzy. With unrealistic future growth assumptions, prices and valuations of underlying businesses become completely detached from underlying fundamentals. Among the drivers of price misalignments today are unrealistic discount rates that assume the cost of capital will remain forever low. Implicit in today’s valuations is the assumption that the Fed can sustain simultaneous high liquidity and low inflation endlessly, which is impossible. There is a business cycle after all. Too much liquidity creates inflation which crimps the real economy. Too much inflation demands removal of liquidity which further catalyzes economic downturns.

A Macro Regime Change Is Upon Us

In the long era of declining inflation and suppressed cost of capital, technology related businesses have conclusively achieved utter dominance in the global equity markets. However, a macro regime change is upon us. Today, we have all the ingredients for a major secular shift in the inflation outlook: fiscal and monetary imprudence, the need to devalue overwhelming debt burdens, chronic underinvestment in basic resource industries, deglobalization, including dis-integration with China, leading to likely long-lasting supply chain disruptions, and a likely secular wage-price spiral. The Covid-19 recession turned out to be a mere blip in what is in all practicality still the longest bull market and largest valuation bubble for both stocks and bonds in US history. The economy is not on sound footing for a new expansion, because there has been absolutely no purging of the excesses from the last one. Today, more than any other time, the continued elevation of these markets requires one factor: excessive liquidity. Investors are starting to connect the dots. We are not talking about the meaningless FOMC dots. We are talking about the idea that persistent inflation could hamstring policy makers from propping up financial markets. This potential macro regime shift places a huge question mark on the sustainability of tech stock supremacy. Just as critical, valuation dislocations caused by long-term shifts in global liquidity also become evident among underperforming assets of the market cycle. Once again, investors have a tendency of deducing that recent market behavior will remain unchanged and excessive pessimism is priced accordingly. Natural resource industries are one key part of the market that remain historically undervalued, especially gold and silver miners. As shown in the chart below, we think we are on the verge of another key turning point in the equity market. We believe there is a strong likelihood of a broad selloff in growth stocks that will likely be accompanied by significant rally in precious metals stocks. The pendulum has swung too far in both directions. The valuation differential of overly hyped technology companies and unloved miners are likely be drastically reduced. Similar to other times in history, these distortions tend to unwind in a vigorous fashion. Note how the growth stocks-to-gold miners’ ratio has been a great barometer of risk in the last 30 years. We saw a similar level of imbalance right at the peak of the tech bubble in 2000. Back then, growth stocks reached unsustainable valuations while precious metals mining companies were in the process of bottoming. Today, however, just in late 2015 and 2018, this ratio is currently at even more excessive levels than what we saw back then.

What Happened To The Business Cycle?

According to data from the National Bureau of Economic Research going back to the Civil War, the average length of the US business cycle is five years. While the length has increased to an average of six years in the post-World War 2 era, there has still been much variation. The last full cycle concluded at the end of February 2020 with the end of the longest-ever expansion and onset of the shortest-ever recession, an almost unbelievable combination. We are now in midst of another expansion. The problem is that due to reckless amounts of fiscal and monetary stimulus, the overindulgences of the last cycle were not eradicated. The bubbles were not allowed to burst. In our analysis, market imbalances today have only become more extreme. At the same time, we have an old problem resurging, inflation, and the Fed is far behind the curve in doing anything serious enough to ensure it is non-transitory. Some of the worst financial market meltdowns on record have been precipitated by necessary policy shifts away from loose financial conditions to combat rising inflation. One of the biggest drivers of the length of the business cycle is long-term inflation expectations. When the Nixon administration untethered the US dollar from gold in 1971, the US was already in a new secular period of rising inflation that began in the latter half of the 1960s as the birth of the Baby Boomers gave way to Gen X. But it did not lead to a series of shortened business cycles (i.e., more frequent recessions) until people became believers in inflation’s staying power, which became the case from 1970 to 1982. During that period, there were four recessions in 13 years. In contrast to Gen Xers, who grew up during a time of rising inflation expectations and frequent recessions, the Millennial generation, born in the latter 1980s through 1990s, was raised during two of the three longest economic expansions in US history. For this generation, business cycles to date have averaged an incredibly long ten years. They have experienced the tailwind of more than three decades of declining long-term interest rates and inflationary expectations. The problem is that now we are in the largest financial asset valuation bubble in US history. The catalyst for its bursting is both the recognition of persistent inflation by workers and investors as well as policy markers’ economic tightening responses in attempts to reduce it.

An Inflationary Transition

After decades of disinflation and low cost of capital, developed economies are currently experiencing a transition that we have not seen in many decades. Countries that have often been used as examples of why monetary and fiscal disorder never leads to inflation, are finally seeing the other side. The most iconic example is Japan, the poster child for an economy mired in deflationary lost decades. Japan’s economy unexpectedly reported its highest print in the price producer index (PPI) in 40 years. Spain, Italy, Germany numbers are even more striking. Their PPIs are now growing at 33%, 27% and 19% respectively. These levels are the most extreme in the history of contiguous data according to Bloomberg, which goes back to the early 1970s, marking a fundamental shift in inflation among developed economies. Yes, we have never seen this level debt accumulation, monetary base expansion, and excessive fiscal spending, but is there more to it? While some may be of the view that inflation was solely due to pandemic issues that are temporary and fixable, we think this issue is significantly more profound. Different than the last 30 years, one of the principal reasons we believe inflation will be sustainable this time around has to do with longer-term trends in capital allocation that have built up over many years already. For a long time, the incremental dollar entering financial markets has almost entirely been allocated into one sector of the economy, technology. The proliferation of index investing has exacerbated this problem. Such investing trends have resulted in a critical problem of preventing capital to flow into basic needs of the economy. In other words, too much money has been chasing exciting information technology projects while essential parts of the economy have been completely forgotten, especially natural resources industries. As shown in the chart below, there has been a major divergence between long-term capex of technology companies versus commodity producers. This is a structural imbalance at the core of the supply chain for all goods and services that began in 2015, long before the Covid Recession.

Five Cents On The Dollar

In our internal discussions with Quinton Hennigh, Crescat’s Geologic and Technical Director, we stumbled onto one fundamental question: When was the last time any of the bigger market cap companies deployed capital into a new mining project of significant size? The answer is, we have not seen any developments of new gold and silver mines by major producers in a very, very long time. Outside of iron ore, the same can be said about large base metals producers. When was the last time Freeport-McMoran, Glencore, Anglo American, Norilsk Nickel, Southern Copper, Grupo Mexico-B developed a large new mining project? Again, not in a very long time. This problem is also evident in the labor market. Everyone wants to be a technologist these days. Software is eating the world today, but people cannot eat software. We see the problem firsthand in our activist fund that is focused on new precious metals mining projects. One of our challenges is dealing with the scarcity of qualified people to run these companies which takes management, technical teams, and workers that have sufficient skills for the industry. It’s a worthy challenge, and we are more than up to it. After a decade of declining college enrollment in the geosciences, we are confident there will be a lot of money to be made by those getting degrees in geology, geochemistry, and mining engineering today. If one is truly passionate about saving the planet also Pipe Dreams and Ponzi SchemesPipe Dreams and Ponzi Schemes, maybe he or she should consider getting a degree in the earth sciences. Keep in mind that the capital conservatism among commodity producers is just part of the problem. What is arguably even more destructive is that effectively for every dollar that has been invested in the global equity markets today just about five cents of it are flowing into commodity producers.

Precious Metals, The Ultimate Deep-Value Opportunity

To put into perspective, even though commodity related businesses make up a small portion of global equity markets today, gold miners are even more extreme. Precious metals companies make up less than 9% of natural resource industries today. While this number is trending higher, we think it’s just the beginning. In our view, gold and silver stocks are the ultimate deep-value opportunity.

Real vs. Financial Assets

This liquidity concept is also evident when we look at long term imbalances between real and financial assets. To revisit an important chart from our friends at Incrementum AG, the commodities-to-equity ratio is now at even lower levels than at other times when we experienced other major macro regime changes, such as the early 1970s and 2000s. Both times we had the US stock market trading at excessive valuations while commodities were at depressed levels. We think this is an “once in a generation” type of opportunity to be positioned on both sides of this imbalance: the long side of natural resource industries while hedging on the short side of ridiculously expensive equities.

Markets Are Running On Fumes

While we continue to see important steps towards investing democratization, the credulity of current market participants when making decisions with their life savings is something truly alarming. Everyone is a genius in a bull market. The overwhelming popularity of investments such as “meme stocks” is evidence that today’s market environment is over the top and running on fumes. The problem at present is especially magnified by the historic high valuation of long duration financial assets. We are not just talking about Treasury bonds. We are also talking about large cap growth and mega-cap tech stocks which are essentially ultra-long duration financial instruments. The valuation of long-duration assets today implies impossibly low interest rates, inflation, and risk premia into infinity, in other words, too low of an overall discount rate. The problem is that too low of a discount rate places far too much weight on far-distant cash flows in the present value calculation. It places far too much faith in the US Treasury and Federal Reserve to maintain low inflation, high liquidity, and the elimination of recessions indefinitely. It is a gross miscalculation. In a recent survey conducted by Bloomberg of the biggest tail-risks for markets in 2022, it is instructive in a contrarian way to see what is at the bottom of the list, i.e., the things people are least concerned about. To us these are the potential black swans. Stagflation and crypto currencies were both at the bottom. Valuations didn’t even make the list! That comes as no surprise. Wall Street and the investment crowd are always looking in the rearview mirror. Inflation at least was at the top of the list. While we agree that the rise in consumer prices is here to stay, we think the risk of a reckoning moment in US equity markets from record valuations is far and away the greatest risk for 2022. As we mentioned earlier, we believe growth stocks are one the most speculative parts of the equity market today. There is a striking divergence between the performance of large and small cap stocks among growth equity indices. Bigger companies have massively outperformed smaller ones, particularly since February. More importantly, note how small caps look to be rolling over. Keep an eye on this, the riskier parts of the market almost always lead the way.

Tech Bubble Parallels

On a daily one-year rolling correlation basis, the disconnection between large and small cap growth stocks is also noteworthy. It is now at its weakest level in 30 years. We saw a similar problem right at the peak of the Tech Bubble in 2000.

Tech, A Crowded Trade

Almost 50% of the Russell 3000 Growth index is now comprised of tech companies. It is important to note, however, that 45% of them were not even profitable in the last twelve months. Another interesting metric related to this, according to JP Morgan, the technology service industry now represents almost 30% of the top 50 hedge funds’ portfolios. Unmistakably, this is a very crowded allocation.

Unprecedented Valuation Distortions

If we dive in further, there are clear indications that within information technology sector, it’s the software industry that concerns us most. Software stocks are almost twice as expensive as they were at peak of the tech bubble. The median stock in this industry now trades at 18 times sales. These valuations are simply unsustainable and clearly priced for perfection. It is as if every company is a disruptor that is guaranteed to be the next Facebook, Apple, Amazon, Microsoft, or Google. What is guaranteed, in our view, is that the future of the industry is going to be a lot more competitive than it has been in the past. We think the average investor today has no clue. The intense competition means that the strong pricing power and profit margins that this industry has enjoyed for so long will necessarily be contracting. Therefore, growth expectations, valuation multiples, and stock prices for the bulk of the companies in this industry are destined to shrink substantially.

40% Of Software Stocks Are Non-Profitable

Today we have the largest percentage of non-profitable software stocks in the history of this industry. This proportion is almost twice what it used to be at the peak of the tech bubble. This is a direct reflection of too many likely undifferentiated companies all trying to be disruptors by competing on low price. As a result, software may be one of the few goods where we are likely to see continued disinflationary pressure, for a while at least. It is also a reflection of the insufficient level of fundamental analysis driving investment decisions and lack of focus by both management and investors on profitability. A coming rise in the cost of capital is likely to change this behavior and drive many of these companies out of business.

Top 10 Largest Stocks Now Trade At 37 Times Earnings

Separately, we often here that our thesis is wrong because this time around the dominant companies in the market are profitable, different than times such as the Tech bubble. We cannot deny the recent strong profitability of the so-called “FAANG” stocks, or the big 5 “FAAMG” in particular. As corporations and individuals accelerated their spending to move to remote work and the cloud, and with ample ammo from the Covid monetary and fiscal stimulus to do so, the fundamentals for these companies have been as strong as they will likely ever be. To us, it screams of a cyclical top in both growth rates and profit margins. We saw the exact same thing with the IT spending surge in 1999 ahead of the dreaded Y2K computer software problem. That was the tech sector’s other boondoggle which precipitated the tech bust in the early 2000s. Our issue is not that today’s tech market cap and profitability leaders are bad companies. They are hugely successful businesses, but that does not mean they do not have cyclical risks. Our main issue is how expensive these stocks are being valued at today. The median price to earnings ratio of the top 10 largest stocks in the US is now as high as it was at the peak of the Tech Bubble, 37 times earnings. Why would anyone want to pay peak multiples on top of likely peak margins and growth rates? It was a horrible move in 2000 and is likely to play out much the same today.

Inflation Is Significantly Higher Than Free-Cash-Flow Yield

Analyzing it more broadly again, if we look at the entire tech sector in the S&P 500 index, these stocks are now more expensive than they were at the peak of the Tech Bubble on a real free-cash-flow yield basis.

Money Losing Stocks Already Rolling Over

Goldman Sachs created an index to track the performance of non-profitable tech companies. Interestingly, after more than quadrupling in prices, this index is now down 26% on a year-over-year basis which is the steepest annual decline since the worst part of the March 2020 crash. We think this indicates a bearish divergence relative to growth stocks at large, where the entire growth index is poised to follow to the downside.

No Fundamental Reason to Invest in Junk Bonds These Days

Continuing to look at the riskier parts of the overall market, junk bonds are perhaps one of the most historically distorted assets out there in our opinion. Net of inflation, high-yield bonds have the lowest real rates in the last 30 years. In investor is paying in the form of negative real yield, for the privilege of accepting default risk. There is no rational case to buy these instruments. This is yet another example of the pure lunacy in today’s markets.

It Is Imperative to Own Tangible Assets

The chart below explains a significant portion of the imbalances that we see in financial assets today, which are quite perplexing to say the least. US money supply surged again by $609 billion just in the last three months. That’s almost seven times its historic average. For the record, this is not a US-only problem. China’s money supply just increased by $840 billion in the last three months. Keep in mind that their highly inflated GDP still is 25% smaller than the US. In our strong opinion, no matter what fiat currency, it is imperative to own tangible assets in this environment.

An Alternative to Fiat Central Bank Currencies

The development of crypto currencies is perhaps the biggest libertarian movement we have seen in history. It is nothing short of a revolution led by a group of individuals fostering similar political ideologies. In some ways, cryptos could be seen as attempts to form new governments if not just central banks. In the crypto world, software programmers and entrepreneurs try to form alternative monetary systems outside the traditional banking and brokerage industries and independent of fiat spewing sovereigns who are prone to debase their legal tender. Crypto is also the Wild West with an abundance of get-rich-quick schemes, hucksters, snake-oil salesman, scammers, con artists, and shills. Whether you believe in the crypto movement or not, this new industry is adding a strong voice against the failures of fiat monetary systems much like the precious metals community has done for centuries. The more popular sound money principles become, the more individuals will be questioning the credibility of currencies backed by highly indebted governments. As insane as it sounds, the most credible central bank balance sheets today are the ones that have built that reputation by owning debt of other massively levered economies. The outlandish part is that the most pre-eminent of these fixed-income instruments is named after the word “Treasure”, which is far from what a boatload of debt really is. The US Treasury does own 262 million gold ounces, which even though it is more than any other sovereign, accounts for less than 2% of government debt. While we are not calling for an immediate return to a gold standard monetary system, we believe that the increasing general public awareness of how untrustworthy fiat currencies become, central banks will be forced to drastically improve the quality of their international reserves in order to restore their credibility. In such scenario, some countries might opt to own crypto assets like Bitcoin. However, more than any other asset in the planet, we think central banks will opt first for gold as it is likely to rekindle its role that it has served for 1000s of years across almost all governments and countries on the planet for that purpose. Central bank accumulation of precious metals is likely to play a major role in driving demand for these assets. While some central banks have started this process already, it is yet to become a new macro trend. The foreign ownership of Treasuries as a percentage of the overall marketable securities outstanding is now 33% and has been in a downward trend since 2008. For now, in nominal terms, federal debt held by foreign investors has been increasing. Therefore, the decline in the chart below has mostly to do with the massive increase in the denominator of this ratio, that being the unprecedented amount of Treasury issuances in the last several years. We think this trend will continue to move lower as central banks become hamstrung to enhance the quality of their international reserves by buying tangible assets like gold in addition to sovereign debt instruments.

The Fed Is Trapped

If the Fed were to raise interest rates back to pre-pandemic levels today, it would invert the entire yield curve.

Inflation is Here to Stay

It is abundantly clear to us that policy makers are still complacent towards inflation. CPI is growing at its fastest pace in 40 years and the Fed still plans on expanding the monetary base for three more months while maintaining short-term rates at zero. More importantly, fiscal spending remains extraordinarily aggressive. When including the current account problem, the government still runs a double-digit twin deficit. The issue is that, if not treated early, inflation can set off disastrous long-term outcomes. The Fed is becoming a slave of the self-created economic imbalances. The destabilizing levels of debt and excessive valuations of financial assets is what handicaps policy makers from being able to meaningfully counter the inflation problem. Different than the times that preceded the global financial crisis, the run-up in consumer prices today is a much broader issue. We are seeing inflation pressure from almost all parts of the economy, particularly from commodity related markets. Nonetheless, it is crazy to think that food prices are already near record levels while agricultural commodities have not even had their big move. The DBA ETF, which tracks soft commodity prices, still is about 35% from their prior highs. We believe there is still a lot of potential for food prices to rise from here and it will likely become the next chapter of the inflation narrative.

A Steep Rise in Food Prices Is Likely Next

We have shown this chart before, but it is an excellent illustration of how ammonia prices have had a very close historical relationship with agricultural commodities which are still ripe for a major move to the upside.

Basic Needs Have Been Forgotten

Back to the inflation theme, long-term changes in labor forces still indicate that we are at the very early bull market stages of a commodity cycle. Also, as shown in the chart below, there is a major divergence in the long-term trend of US nonfarm payrolls between tech related jobs versus natural resources and mining. A similar distortion marked the beginning of a commodities bull market and the peak in overall equities in early 2000. This chart also portrays the extraordinary amount of capital and labor that has been continuously chasing the technology sector while ignoring opportunities in critical parts of the economy, such as natural resource industries.

The Unintended Consequences Of ESG Policies

In addition to the lack of capital liquidity flowing into commodity related businesses, there is also a major political effort to prevent natural resource companies from exploring, developing, and producing valuable necessities. To be specific, the energy industry has been painfully impacted by these policies. Oil and gas rig count is still lower than it was at other major bottoms for energy commodities. This is a clear indication of an energy cycle at its early innings. These are the unintended consequences of ESG policies, though some may argue it was intentional. The setup for rising commodity prices, nevertheless, is probably the fattest pitch that commodity investors are ever going to get.

A Secular Decline In US Job Quality

Aside from supply disruptions, cost push inflationary forces have also been driven by a pronounced shift in labor cost. Related to this, JQI assess the overall health of the US jobs market and has reported that US work quality among the private sector has been in a steady decline for over 30 years. This is a reflection of dissatisfaction of workers about their wages and salaries. It will likely result in a sustainable increase of workers’ remuneration that has already started.

The Value Of Global Macro Investing

Crescat is a value-oriented global macro firm with three differentiated hedge fund strategies: Global Macro, Long Short and Precious Metals. Our Precious Metals fund returned 235% net in its first year ending in August 2021 while gold prices declined almost 10% during this same time frame. This strategy has built over 70 activist positions in some of the best exploration companies around the globe at highly attractive valuations after a decade-long bear market. Our portfolio companies have already made at least ten bona fide new discoveries likely to become 2+ million ounce producing mines each. Meanwhile, we have what we would consider another 20 or so incipient discoveries in the works, and at least 40 more exciting exploration projects. Crescat’s activist investments in total have helped to fund exploration programs currently targeting over 300 million gold equivalent ounces. To put this into perspective, the US Treasury, as we indicated above, the largest owner of gold in the world owns a mere 262 million ounces. Our goal is to build the next generation of large-scale, high-grade resources in viable jurisdictions. To put it simply, we are buying highly economic gold and silver in the ground for literally pennies on the dollar. Our edge is the ability to leverage proprietary equity and macro models, combined with unparalleled industry expertise from our world-renowned exploration geologist, Dr. Quinton Hennigh, Crescat’s Geologic and Technical Director. Separately, Crescat’s Global Macro and Long/Short funds, which are also significantly invested in gold and silver companies, offer exposure to other major macro themes that we have identified. Both of these strategies made Bloomberg’s top 10 hedge funds list for 2020 after delivering gains during the March downturn via our short positions and by continuing to accrue profits through year end from our deep-value commodity related longs. With inflationary pressures rising in the US, we believe investors will be rotating out of over-valued long duration financial assets and into undervalued commodity cyclicals and inflation hedge assets, such as scarce natural resource stocks. We call this overriding theme “The Great Rotation”. Going forward, we intend to capitalize from a long overdue correction in long-duration asset prices and the likely more pernicious peak of the US business cycle still to unfold. We believe the pandemic driven recession was just a blip and the opportunity to profit from today’s asset bubbles are even more timely. Therefore, our Global Macro and Long/Short funds have significant short positions in overvalued large cap growth stocks among other overvalued equities, and longs in undervalued tangible assets, including companies that own and produce them. As part of our investment process, we apply value principles through our proprietary quantitative models to help us select and manage a diversified list of positions. Our Global Macro fund is further differentiated by currency and fixed income positions supported by extensive research. These positions include substantial short exposure to the Chinese and Hong Kong currencies versus the US dollar by being long call options in USDCNH and USDHKD. Additionally, we are short high-yield bonds, US 10-year Treasuries, and 10-year German bunds, through long put options.

Performance

Download PDF Version Sincerely, Kevin C. Smith, CFA Member & Chief Investment Officer Tavi Costa Member & Portfolio Manager For more information including how to invest, please contact: Marek Iwahashi Client Service Associate miwahashi@crescat.net Cassie Fischer Client Service Associate cfischer@crescat.net Linda Carleu Smith, CPA Member & COO lsmith@crescat.net © 2021 Crescat Capital LLC Article by Crescat Capital2,2651

NEVER MISS THE NEWS THAT MATTERS MOST

ZEROHEDGE DIRECTLY TO YOUR INBOX

Receive a daily recap featuring a curated list of must-read stories.Show CommentsWelcome, stevesalgadoProfileLog outToday’s Top Stories+Hot TakesCourtesy of the Market Ear

Upgrade to Premium. Real-time around the clock feed that focuses on the important things that move stocks and markets. For professional traders.1d ago at 10:03

TME Saturday: thank God it is a quiet weekend

See TME’s daily newsletter email below. For the 24/7 market intelligence feed and thematic trading emails, sign up for ZH premium here.

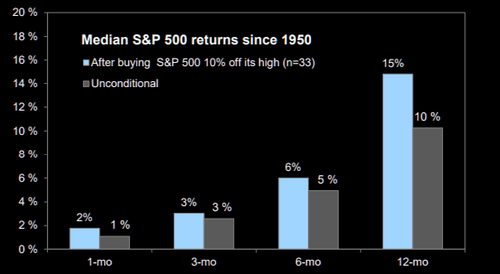

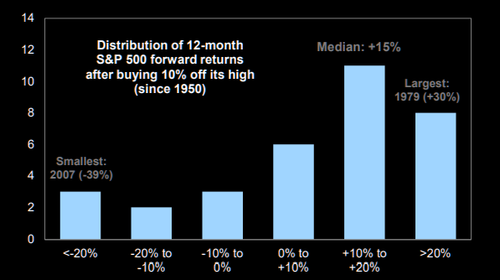

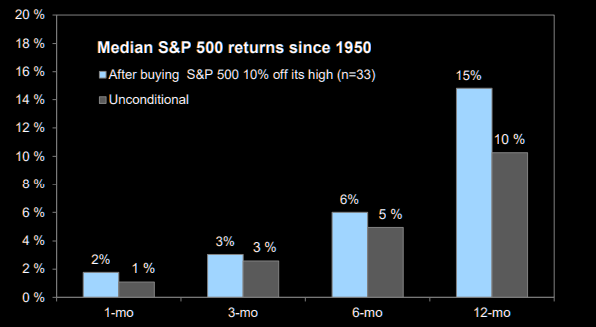

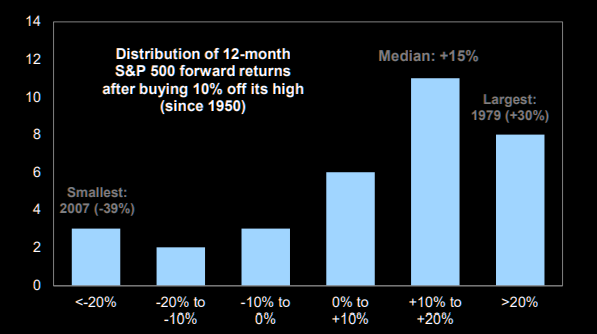

Buy-the-dip: working great since 1950

Past S&P 500 corrections have typically been buying opportunities. Chart 2 shows distribution of 12-month S&P 500 returns following 10% declines.

Source: GIR

Source: GIR

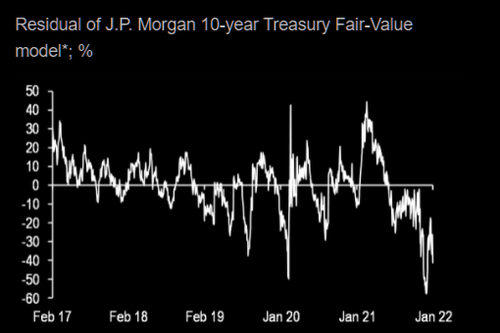

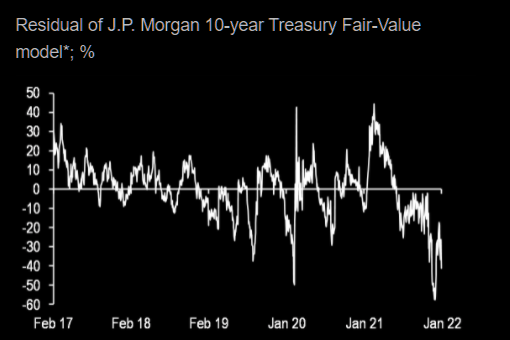

10-year Treasuries expensive again

Given the repricing in Fed and inflation expectations this week, 10-year Treasuries appear quite expensive once again.

Source: JPM

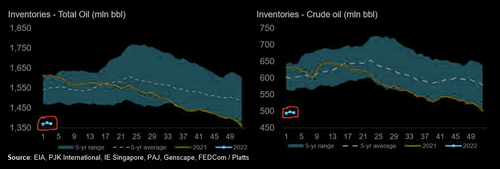

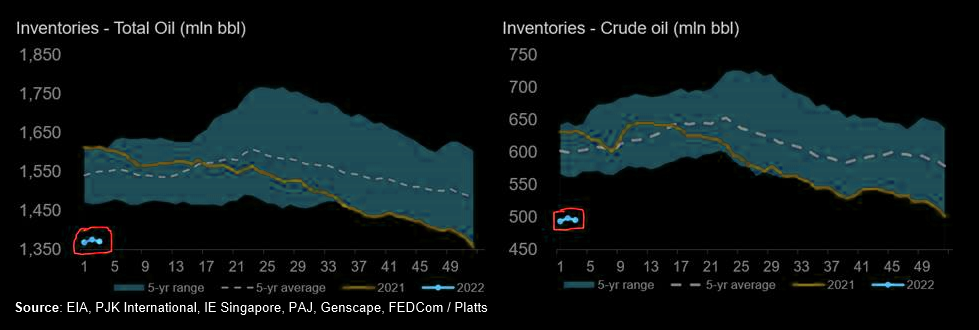

Oil loves war

As MS Research pointed out earlier this week, geopolitical risk is typically a tailwind for commodity prices, given disruptions tend to impact supply far more than demand…Global oil inventories dipped -4.8mm bbls WoW, with both crude and product stocks drawing counter-seasonally, and remain well below the 5yr range. Crude stocks drew by -2.9mm bbls (including the US SPR changes), while product stocks drew by -1.9mm bbls.

Source: EIA

Corporate credit market have been rather resilient

Historically, credit markets have been a leading indicator for equity investors in times of recession or large drawdowns, however this time has been the quite the opposite. IG and HY credit has held up quite well with total returns (through Thursday) of -3.2% and -1% vs. S&P -9.2% and NDX -14.2%. For context IG OAS is 104bp (24bps off tights) and HY OAS is 332bps (70bps off tights). The resilience can be attributed towards healthier BS and cap structures post COVID and thus, more resilience to rate shocks than other duration assets. The argument for further deterioration in IG and HY from here depends on the linger growth slowdown may come with a hawkish Fed.

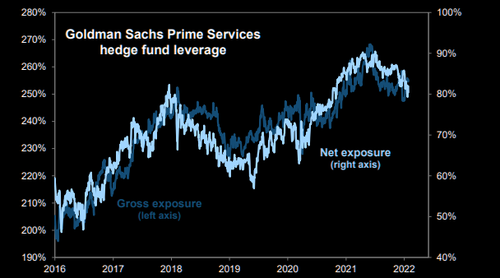

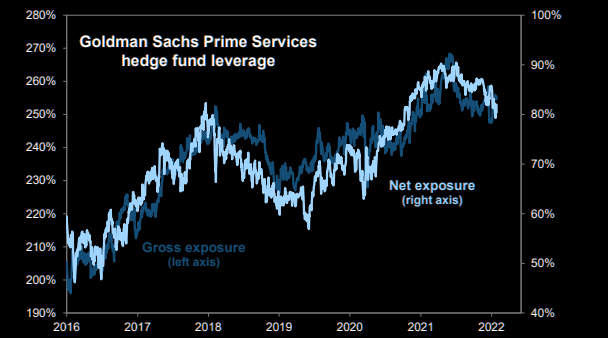

Hegde funds: half full half empty

HF leverage at 1-year lows but above 3- and 5-year averages.

Source: GS Prime Brokerage

Hedge fund horror

Crowded long alpha in North America is having its worst start to the year since the Morgan Stanley PB Strategic Content team began tracking the data in 2010; the names are down ~19.2% YTD. With that said, the crowded shorts in North America fell ~5.4% this week, but hedge funds hold nearly ~2x more exposure to the crowded longs in N. Am compared to the crowded shorts (MS).

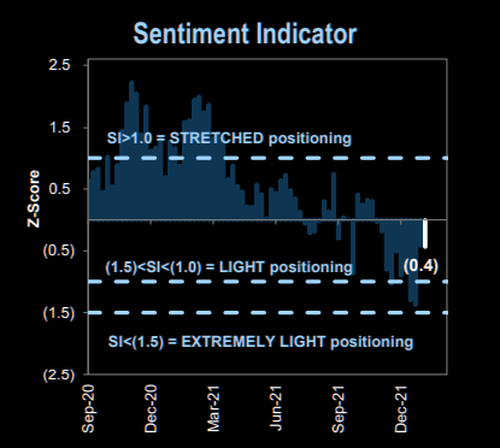

Sentiment: buy signal gone

Sentiment half full half empty….The GS Sentiment Indicator measures stock positioning across retail, institutional, and foreign investors versus the past 12 months. Readings below -1.0 or above +1.0 indicate extreme positions that are significant in predicting future returns.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}