Source – lewrockwell.com

- “…Our overlords wouldn’t intentionally crash the economy, would they? Let’s take a look. For context, the Federal government is being warned by Janet Yellen at the Treasury Department that if Congress doesn’t vote to lift or suspend the debt limit the country will go into default. The nation runs out of cash on Oct. 18. Never before has this issue been grandstanded as much as it is this year”

Is The Economy Being Crashed On Purpose? – By Bill Sardi

Imagine you are on a cruise ship and you secured your valuables with the ship’s purser. And later you see the purser hurriedly getting on a lifeboat with canvas bags used for holding valuables. What kind of a signal would that send to you?

It would appear to me the ship is about to sink and the purser is trying to take everybody’s money with him as he rescues himself. Now recognize, the purser could say he was just making sure everyone’s valuables were saved should they survive the sinking or at least preserve passenger valuables for their heirs, in what would be plausible denial. Or who knows, maybe he will say it was just a drill.

Now to assess a real occurrence.

Two top officials at the Federal Reserve bank resigned a few days ago over revelations they were extensively trading stocks in 2020 when the FED was spending trillions of dollars to stabilize financial markets. The investments were permissible under the FED’s rules, but there certainly appears to be a conflict of interest. One of the perpetrators made trades worth over $1 million in 22 stocks and index funds. These are insiders with advance info about market conditions.

You might come to the same conclusion that “the boat is sinking,” as I did in my imaginary story about the purser on a cruise ship. Who is going to penalize these bankers if the ship sinks? They know there isn’t time for them to be penalized. What do they know that we don’t know?

What other signs do we have of a sinking economy?

There is a country where many of CEOs of major companies took their payouts the bonuses, and resigned, in an unexplained move. Were they getting off a sinking ship early? That country is the United States.

A report by Global Research said: “top corporate executives (over 1600 of them in 2020) were dumping billions of dollars-worth of shares in their own companies just before the market completely cratered.” That was prior to the March 2020 pandemic announcement. Again, what did they know?

Is the ship of state being sunk intentionally?

Our overlords wouldn’t intentionally crash the economy, would they? Let’s take a look.

For context, the Federal government is being warned by Janet Yellen at the Treasury Department that if Congress doesn’t vote to lift or suspend the debt limit the country will go into default. The nation runs out of cash on Oct. 18. Never before has this issue been grandstanded as much as it is this year.

This finance stuff is over the heads of most Americans. It uses lingo like “margin call,” “federal funds rate,” “balance sheet,” “equity,” “liquidty,” “quantitative easing,” “GDP.” The public just hopes others entrusted to look out for their financial welfare are doing their job.

The budget battle of 2021

After some tumultuous disagreements, the House of Representatives voted to suspend the nation’s debt limit until Dec. 2022. Government punted. Yet it all seems like an orchestrated game. Like they are trying to put the public on edge. Neither political party wants to take the blame for an economic collapse, which appears inevitable.

Look at the Dow Jones Industrial Index

As you examine the Dow Jones Industrial Average in the chart below for the period 2016 to 2021 (click on the chart to see it in blown up view), we see just how the stock market is rigged.

By the way, can you remember when a 10,000 Dow was unheard of? Now we are at 34,000 Dow. This is more than a bubble, it is the Lawrence Welk bubble machine.

The chart reveals for every crash of the stock market, there was a correction. Wall Street is very adept at keeping the market profitable and turning yields for pension plans.

To achieve this unprecedented growth in the value of stocks, the Federal Reserve bank simply began flooding the economy with money so investors could buy stocks. By the Federal Reserve paying such a low rate of interest on safer government bonds, investors were forced to make riskier investments and buy stocks.

But now over $4 trillion of money has been created by the central bank and the Dow rose to 34,000. The next correction will predictably be downward (see chart below).

Turn in direction: increase yield on bonds to drive investors out of stocks

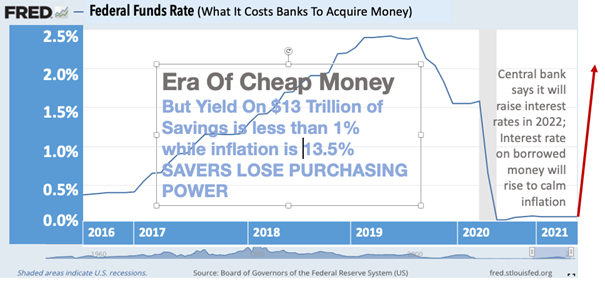

As if to aid and abet the problem, the central bank now says it fears inflation (more money dilutes the value existing money if productivity remains the same) and the FED is going to raise the rate of return (interest rate) on federal government bonds (US Treasury Bills, maybe up to 2.5% by next year).

The current Federal Funds Rate (what commercial banks pay as a premium to acquire money from the central bank) is near zero (see chart below). This means borrowing money has been cheap. People have been able to buy homes and automobiles at very low rates of interest. The housing market and home values have been propped in this manner also.

Era of cheap money is over; housing and stock markets have been propped

The problem is, while it is cheap to borrow, interest rates (rate of return) on banked money is less than 1%, while inflation (loss of purchasing power of money) is rising.

The Federal Reserve Open Market Committee says inflation is percolating at ~3.7% in late summer of 2021. The target inflation rate established by the FED is ~2%. But you can’t rely on government numbers. None of them are real. Certainly not this one.

ShadowStats.com says, if the rate of inflation were calculated like it was done in 1980, then the consumer goods inflation rate is more like 13.5%. (See chart below)

There is $9 trillion of money in US savings accounts that is losing over $1 trillion of purchasing power a year. Savers are being robbed while they sleep.

Right now, Americans not only pay income tax, and Medicare and Social Security taxes taken out of their paychecks for future medical care and pensions, but they also are paying a steep inflation tax (~13.5%) on their saved money.

Federal government revenues vs. spending

Annual federal government tax revenues are ~$3.9 trillion and spending is ~$7 trillion a year. That is how the US accumulated a $28 trillion national debt. America is living a lifestyle it hasn’t earned.

But now, after pumping $5.4 trillion into the economy since March of 2021, Congress is voting on dumping another $3.5 trillion on top of the $28 trillion of accumulated national debt. Oh, hell, everybody close their eyes, and just print more money, like Congress has done in the past, as if there is no debt limit.

What will foreign investors do with their Treasury Bonds?

One of the ways the US creates more money is to borrow from foreign countries and offer them a US Treasury Note (an IOU) in exchange. But wait, if the US keeps doing this, spending more money than it collects, at some point other countries will completely back away from buying US Treasury bonds, which is the current circumstance, because we are never going to be able to pay back our debts (trillions of dollars to China and Japan).

Foreign investors have been forced to the stock market because of such low yields on US Treasury Bonds. But now foreign investors may get lured back into bonds.

Dissent

Here is where things really get sticky.

US Senator Joe Manchin (D-WV) says he can’t support $3.5 trillion more money printing when we can’t even pay for essential social programs like Medicare and Social Security. (Did you hear that? Medicare and Social Security are broke.)

Banks get free shot in the arm

The $4 trillion of aid money issued by the Federal Government, about $2.3 trillion went to businesses, $651 billion in tax breaks, $454 billion to the Federal Reserve itself, $670 to the Payroll Protection Plan, and $884 billion (one-fifth of relief money) went to help workers and families.

The $2 trillion gift that your banker is holding

Congress simply sent ~$2 trillion of direct to American citizens, but those deposits hit the banks and buoyed their deposit accounts. Recipients didn’t go out and spend all that money. Banks are using it as reserves. Some recipients paid off credit cards and others just sat on it. So, the extra money didn’t boost the consumer economy. The banks got a free shot in the arm.

Reserve requirements abandoned (yes, really!)

In the recent past too-big-to-fail large banks were to hold another 3% in extra reserves over and above the 10% they are required to keep in reserve. But as of April 2021, that 10% reserve requirement has been abandoned, leaving only saving accounts covered by the Federal Deposit Insurance Corp. (FDIC) to cover losses in case of a bank run. That extra 3% big banks were supposed to keep in reserve has also been nixed. If the mother of all bank runs materializes, don’t expect anything but a financial wipe out.

Only backstop left

The only backstop is the Federal Deposit Insurance Corp. should a banking crisis occur. The FDIC insures savings accounts up to $250,000. The FDIC holds about $120.5 billion as of the 2nd quarter 2021 against $8.2 trillion in insured deposits (1.7-cents on the dollar). Are American savers being set up to be completely vanquished of all their money?

Revenues vs. spending

Federal tax revenues for 2021 are projected to be ~$4.174 trillion, with 6,011 trillion in spending, which would add $1.873 trillion to the $28 trillion accumulated national debt. More than 65% of the $6,011 trillion pays for Social Security, Medicare and Medicaid, out of the general fund, as those trust funds are insolvent except for FICA payroll deductions every two weeks.

The US pays interest on its debt, about $378 billion/year (2.2%), but this is about spike much higher (~2.5% in 2022) as interest rates on money are going to rise to prevent run-away inflation. Taxes would have to be raised to pay the interest, that is, unless the US defaults.

Supply chain problem created by the central bank

While Federal Reserve Chairman Jerome Powell is quoted to say: “it is frustrating to see the bottlenecks and supply chain problems not getting better,” it is the free money supplied to unemployed Americans that kept workers from going back to work and created this problem. Chairman Powell’s finger of guilt should be pointed at government that created the supply chain problems. Are they scuttling the ship intentionally?

They paid the deck hands and the stewards on board the ship enough money to stay onshore. The boat is about to sink without a crew on board to usher everyone to the life boats.

Bottom line: what will happen?

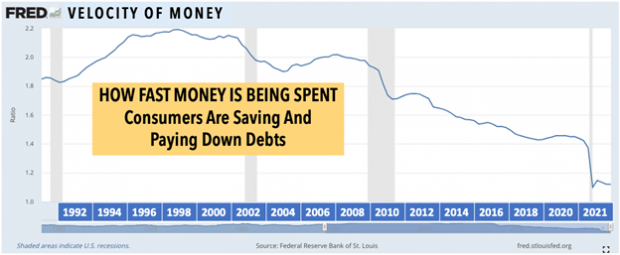

1. The nation’s central bank says it will begin to pay more interest on US Treasury Bonds, which tightens credit and calms consumer spending, which isn’t happening anyway. The velocity of money (how fast money is spent from butcher to baker to candle-stick maker) is at an all-time low (see chart below). Because consumers haven’t been spending, anticipated inflation has not been experienced yet.

However, prices are now rising as I am writing this report. A large paper box supplier just raised prices 13-15%. A local supplier reports wood pallets which cost $8 are now costing $80.

As the central bank provides safety and a higher yield on its US Treasury Bonds, investors will be lured to buy these bonds and move their money out of the stock market, which is over-priced (think bubble machine is going to blow up).

- Taxes will rise. Globalists, who are involved in a covert takeover of the US as I write, say digital money will generate another trillion dollars in federal taxes. Digital money will eliminate the need for street-corner banks. More money for the federal government and less costs for banks. But none of this really benefits Americans who will enter an era of irreversible serfdom.

Americans refuse to be taxed for these benefits

A news report says 71% of Americans claim they won’t support a $3.5 trillion “reconciliation package” if it increases their taxes. But under a digital currency system, the citizenry will have no vote.

The US Treasury Department’s Janet Yellen says a “a shocking $7 trillion is taxes is going uncollected.” These proposed taxes are really targeting the middle class, not the wealthy. Government wants to collect more so it can control more. You might say, $7 trillion of freedom will be deducted from the citizenry.

The Great Reset; digital vs. paper money

Put your thinking cap on. The European-based World Economic Forum is working feverishly to take advantage of the COVID pandemic (“never let a good crisis go to waste”- said Saul Alinsky in his Rules for Radicals) and usher in THE GREAT RESET, a covert overthrow of the capitalist, Constitutional, free-market, free-enterprise, Judeo-Christian work ethic, freedom of speech-religion-right to bear arms country, and currency system, all under the guise a deadly virus that mutated just on time, after a cadre of business executives and public officials conducted a drill over an outbreak of the very same virus. (Just a coincidence?).

The Great Reset calls for abandonment of history, religion, sovereign borders, equity rather than liberty for all. There will be no personal property or wealth; everything will be rented (houses, autos, vacuum cleaners, lawn mowers, etc.). Paper money will be replaced by a digital currency issued directly from the government that would approve or deny all transactions. And the International Monetary Fund, The World Bank, the United Nations, World Health Organization, along with private enterprise like Blackrock, Microsoft, Mastercard, are all in for THE GREAT RESET. These are the covert insurrectionists. They should be put on trial for treason.

John F. Kennedy talked about them in his speech delivered to the nation’s news press. Here are JFK’s words uttered 27 April, 1961 (my comments in parentheses):

…there is little value in insuring the survival of our nation if our traditions do not survive with it (history is now being erased). And there is very grave danger that an announced need for increased security will be seized upon by those anxious to expand its meaning to the very limits of official censorship and concealment (censorship of the internet)….. Our way of life is under attack. Those who make themselves our enemy are advancing around the globe. The survival of our friends is in danger. And yet no war has been declared, no borders have been crossed by marching troops, no missiles have been fired.

For we are opposed around the world by a monolithic and ruthless conspiracy that relies primarily on covert means for expanding its sphere of influence—on infiltration instead of invasion, on subversion instead of elections, on intimidation instead of free choice, on guerrillas (BLM, ANTIFA) by night instead of armies by day. It is a system which has conscripted vast human and material resources into the building of a tightly-knit, highly efficient machine that combines military, diplomatic, intelligence, economic, scientific and political operations.

Its preparations are concealed, not published. Its mistakes are buried, not headlined. Its dissenters are silenced, not praised. No expenditure is questioned, no rumor is printed, no secret is revealed. It conducts the Cold War, in short, with a war-time discipline no democracy would ever hope or wish to match.

The US economy is primed to fall. The Wall Street Journal is not going to tell you this. A humongous depression far greater than the depression of the 1930s, is planned. And in so doing, the masses will beg for the digital currency as the only way out. A date will be established to turn in paper money, maybe even at less than face value. Notice coins were tagged as carriers of the virus, to be turned back in to banks. Paper money banished as a medium of viral transmission.

Those in power make it appear they are sending Americans free money, they are rescuing you, from the COVID, from joblessness, from the sinking ship. In fact, the citizenry is being set up for a big fall. And most Americans are none the wiser.

Copyright © Bill Sardi, writing from La Verne, California. This article has been written exclusively for www.LewRockwell.com

Reblogged this on Vermont Folk Troth.

Reblogged this on muunyayo • trial by combat….