Source – zerohedge.com

- ” …CPI inflation has remained tame leaving many participants persuaded that we’d somehow transcended inflation…This will turn out to be wrong…I wrote about about the inflationary collapse of the Soviet Union, where inflation took off sharply almost overnight….Warren Buffett warned that for a debtor nation, inflation was the economic equivalent of the hydrogen bomb”

The coming inflation tsunami and how to protect your portfolio

Warren Buffett warned that for a debtor nation, inflation was the economic equivalent of the hydrogen bomb. Runaway inflations tend to emerge when an economy’s debt burden becomes unsustainable usually as a consequence of too much government spending and too much war. For a while now, nearly all categories of debt in the U.S. economy have been breaking records: government, corporate as well as household and student debt. Worse, the levels of delinquency have been rising and credit standards have been deteriorating, particularly for corporate debt. And with the insane public health response to this year’s Covid 19 pandemic, the government has ramped up deficit spending and the Fed its printing presses to unprecedented rates.

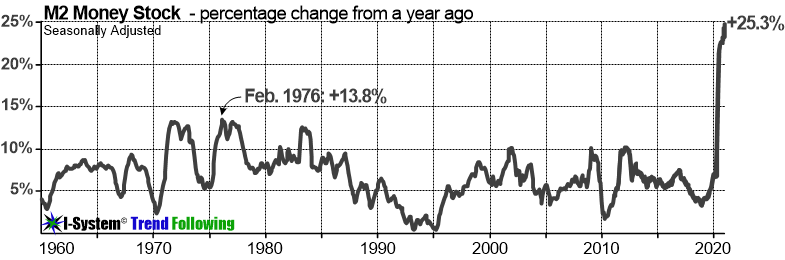

Meanwhile, the CPI inflation has remained tame leaving many participants persuaded that we’d somehow transcended inflation and that it was no longer a risk. This will turn out to be wrong. In one of my previous articles, I wrote about about the inflationary collapse of the Soviet Union, where inflation took off sharply almost overnight. That episode is far from irrelevant to our situation today. In “Dying of Money,” Jens Parsson documented certain aspects of the 1923 German hyperinflation that should equally concern us from today’s perspective. German inflation took off in the summer of 1922 and peaked in November of 1923. But that unravelling had gestated for some eight years prior, the ultimate result of debts accumulated through war spending and mounting post-war government spending.

Prosperity before the unravelling

As the debt burden grew, German economy even had a remarkable boom period in 1920 and 1921. Basing his account on the testimony of journalists and economists who lived through the period, Parsson conveys the mood of that time: “Industry and business were going at fever pitch. Exports were thriving… Hordes of tourists came from abroad. Many great fortunes sprang up overnight. Berlin was one of the brightest capitals in the world in those days. Great mansions of the new rich grew like mushrooms in the suburbs. The cities… had an aimless and wanton youth and a cabaret life of an unprecedented splendor, dissolution, and unreality. Prodigality marked the affairs of both the government and the private citizen.” Unemployment was virtually non-existent and profitable speculation in the stock markets became one of the nation’s foremost obsessions. “The volumes of turnover in securities on the Berlin Bourse became so high that the financial industry could not keep up with the paperwork, even with greatly swollen staffs of back-office employees, and the Bourse was obliged to close several days a week to work off the backlog.”

So, for a while, German economy was booming, the place appeared prosperous (while the rest of the world was enduring a severe recession), stock markets soared and consumer prices remained stable in spite of the feverish activity, rising government spending and a gaping current account deficit. The exchange rate of the mark against the dollar and other currencies actually rose for a time, and the mark was momentarily the strongest currency in the world.

Still, many analysts of the time sounded alarm about the mounting post-war debts and the government’s lax fiscal discipline. The cabinet of Prime Minister Matthias Erzberger tried to tackle the problem by curtailing government spending and drastically increasing taxes, but these unpopular measures were not sustainable in Germany’s young democracy. Part of the pundit class of the day argued that deficits didn’t’ matter and that inflation wouldn’t escalate out of control because it seemed tame at the time. The nation’s wealthy investor class rebelled against Erzberger’s tax regime and soon he was forced out and replaced by Karl Helfferich who reversed Erzberger’s taxes and reopened the flow of easy money (this is what brought about the boom of 1920-1921).

However, inflation ultimately did catch up with the German consumer prices. All at once and seemingly out of nowhere inflation took off in the summer of 1922. In the four months from July 1922 consumer prices rose tenfold and two hundred-fold in 11 months. In late 1923 prices were at least quadrupling every week. The mystery we should all ponder today is, where was inflation up to that point and what made it burst out so suddenly and so violently, catching nearly all by surprise?

Reichsbank’s easy money policy seemed entirely beneficial and controlled at first. The German economy appeared healthy and prosperous for a time. Monetary inflation was being absorbed by the stock markets and by foreign investors (the root cause of Germany’s large current account deficits). Writes Parsson: “Until 1922 and the very brink of the collapse, Germans and especially foreign investors were absorbing marks in huge quantities. Only the international reputation of the Reichsmark, the faith that an economic giant like Germany could not fail, made this possible. … investor’s willingness to save marks kept the marks from being dumped immediately into the markets, and thereby for a long while held prices in check. The precise moment when the inflation turned upward toward the vertical climb was undoubtedly timed by no event but by the dawning psychological awareness of the German and foreign investor that Germany was not going to back its money. With that, the rush to get out of the mark was on. Like a dam bursting, the seas of marks flooded into the markets and drove prices beyond all bounds.”

With this in mind we can revisit the coordinated policy of “financial repression” by the G7 central banks in the aftermath of the 2008 financial crisis and the bailout of the too-big-to-fail banks. This policy was necessary to ensure that the massive new bailout funds remain confined to capital markets at low interest rates and to keep them from spilling over into the economy. Ten years later we can see the results in the “everything bubble” which, but for this year’s large correction is inflating on and on. At the same time, CPI inflation really has remained tame – and for far longer than many of us believed it could.

However, as Parsson warned: “A buoyantly rising stock market marks the opening stages of every monetary inflation. A sharply rising stock market proves to be an unfailing indicator of monetary inflation happening now, price inflation coming later, and a cheap boom probably occurring in the meantime. … Stock market speculation is a principal relief valve concealing latent inflation pressure. Booming stock market prices are themselves a form of price inflation, normally the most inflated of all, but never thought of as such. … The stock market therefore relieved pressure temporarily from inflation elsewhere. The government had artificial devices for locking money into investment, such as its growing supplies of government debt and the tax inducements drawing money … into pension funds, and these government dikes around investment markets stored up inflationary potential in great brimming reservoirs and out of harm’s way.”

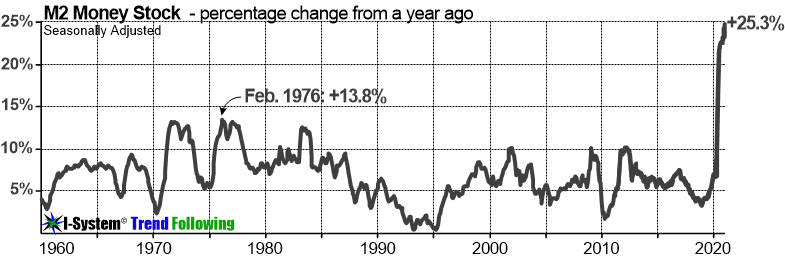

Today, as in 1920s Germany many economists have declared that debts and deficits don’t matter, that inflation wouldn’t happen and that the current levels of prosperity constitute proof that the economy is healthy and risks under control. But we should not remain complacent. Our commentariat and pundit class rarely expect surprises and significant changes in inflation almost always come as a surprise. Already in 2012 Paul Singer intimated that a rapid onset of inflation was one of his greatest worries: “The first whiffs of either commodity inflation or wage inflation… might cause a self-reinforcing set of market events … which may include a sharp fall in bond prices, … fall in stock prices, rapid increase in commodities…” And where are we today? Not long ago, none other than Alan Greeenspan warned that, “Right now, there’s no real inflation at play. But if we go further than we are currently, inflation is inevitably going to rise.” Greenspan spoke those words on 17 December 2019 and since then we’d gone much, much further than we were:

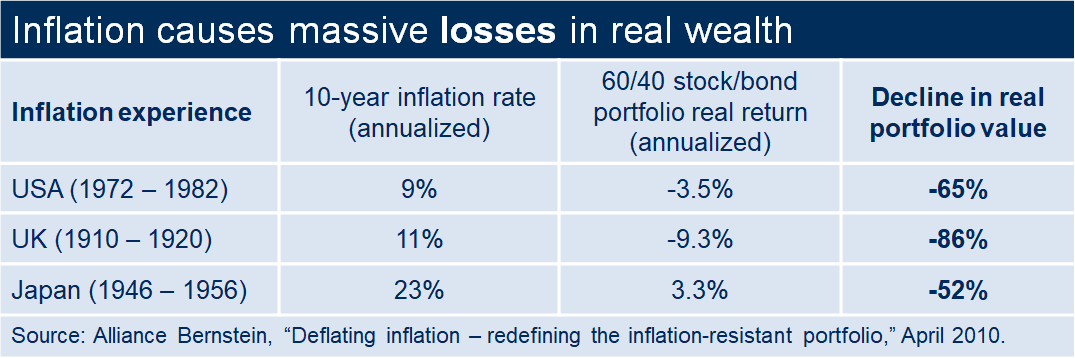

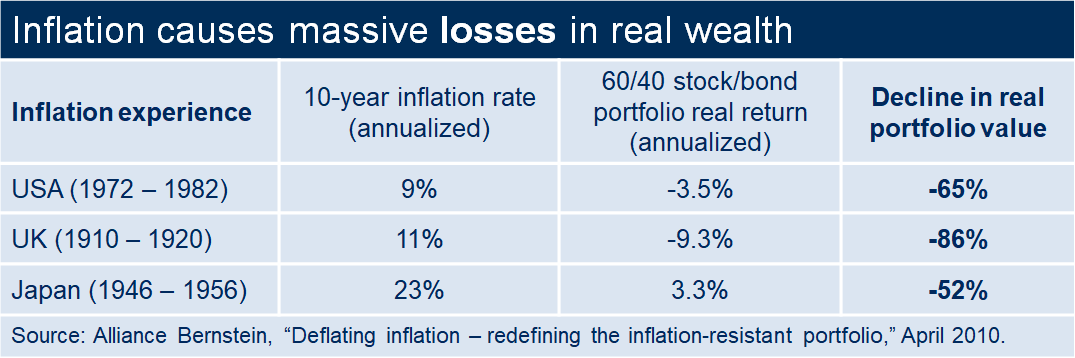

So if the maestro is right, it would appear that inflation is inevitably going to rise. This should not come as a surprise. Inflations have been pervasive in the age of central banking. According to Stanley Fsicher‘s “Modern Hyper- and High Inflations,” since 1960, more than two thirds of the world’s market economies experienced episodes of inflation of 25% or higher. On average, investors lost 53% of their purchasing power during such episodes. In many cases, the losses were much worse. During the 1970s inflation, US investors lost as much as 65% in real terms.

In some episodes, like Weimar, the losses came close to 100%. When exactly the price inflation might rise, how fast and how long it will run is anybody’s guess. We are living through an unprecedented monetary experiment and drawing any parallels from the uncharted waters we are now sailing through is bound to be guesswork. “The unnerving quality of an inflation,” wrote Parsson, “is that no one knows anything for sure.” With regards to the American inflation, he concluded prophetically in 1974: “… even if the nation’s inflationary plight was not yet so grave as it had been in other lands at other times, in the fullness of time it would be.”

How to hedge against inflation?

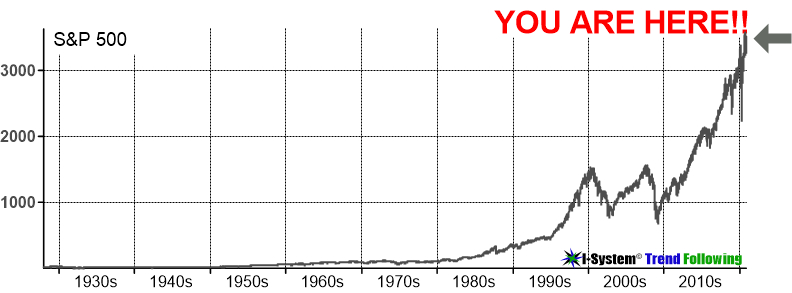

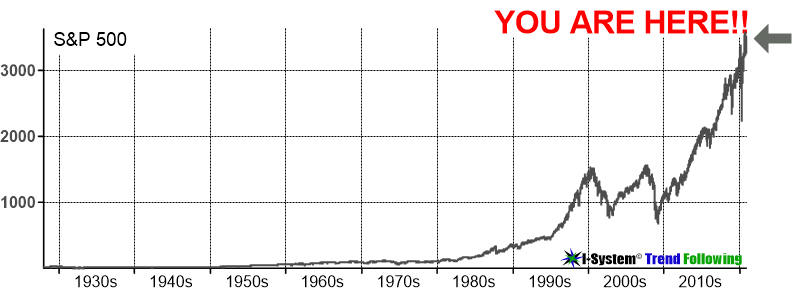

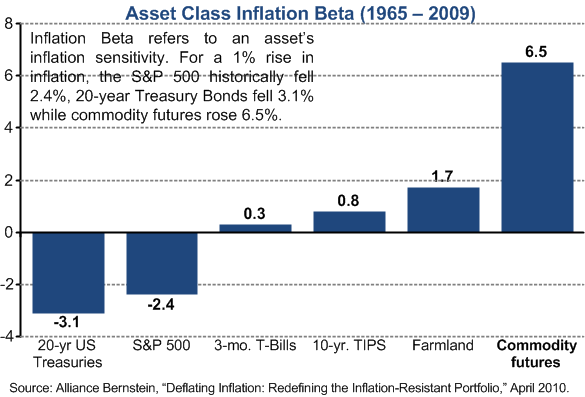

So, what’s the investor to do? Of late, the commentariat has been generous with advice – some of it good and some quite awful. It tends to be Gold, Bitcoin, real-estate, stocks, inflation-indexed treasuries, farmland, commodities, cyclical stocks, mining stocks, etc. On the qualification of having spent eight years of my life running an inflation hedging fund during which time I read every book and research report on inflation I could lay my hands on, there’s a good case to be made for gold and silver. Farmland could also be a sensible investment, but do stay away from residential and commercial real estate. Months ago I would have agreed that Bitcoin was an excellent inflation hedge as well, but at today’s prices I’m no longer as confident. I should say the same about equities too:

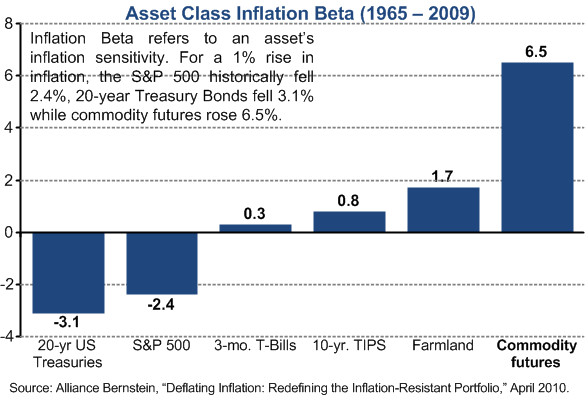

I do believe however, and a number of empirical studies confirm this, that the best hedge by far is a diversified commodities futures portfolio that includes energy, industrial and precious metals, major agricultural commodities, commodity currencies (AUD, GBP, NOK, MEX, BRZ, ZAR, RUB – and yes, why not, BTC in this mix). More about this type of hedge and how to construct a diversified futures portfolio at this link.

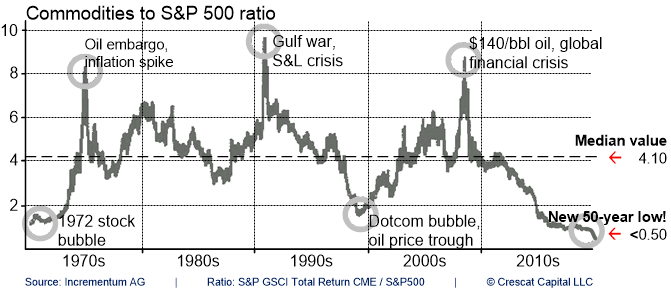

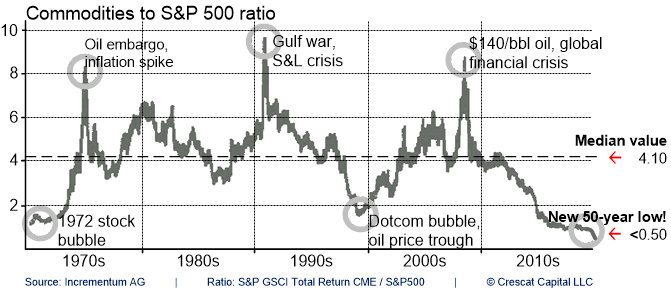

Another reason to consider commodities is that during the 10+ years of quantitative easing, it has remained conspicuously depressed and in this sense offers perhaps the only true diversifier:

Either way, the future promises a bumpy ride. Business as usual investment management will prove difficult and fraught with risk.

Alex Krainer – @NakedHedgie – former hedge fund manager, creator of the I-System trend following and founder of Krainer Analytics. PDF: I-System Diversified Trends Program: Protecting Your Portfolio Against Inflation and Stock Market Collapse. Author of the 5-star rated book, “Mastering Uncertainty in Commodities Trading” and “Grand Deception: The Browder Hoax” (Kindle/PDF, paperback), which was twice banned on Amazon by orders of swamp creatures from the U.S. Department of State. Occasionally writes at TheNakedHedgie.com. Views and opinions not always for polite society but always expressed in sincere pursuit of true knowledge and clear understanding of concepts and phenomena that matter

The coming inflation tsunami and how to protect your portfolio | Zero Hedge | Zero Hedge

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Deficit spending is alleged to be, dollar for dollar, a value of profit on the ledgers of Manhattan finance institute.

Ref. https://ppjg.me/2019/11/18/the-federal-reserve-a-different-view. FEDERAL RESERVE; A DIFFERENT VIEW