Source – canadianpatriot.org

- “…“What if a small group of world leaders were to conclude that the principal risk to the Earth comes from the actions of the rich countries? And if the world is to survive, those rich countries would have to sign an agreement reducing their impact on the environment. Will they do it? The group’s conclusion is ‘no’. The rich countries won’t do it. They won’t change. So, in order to save the planet, the group decides: Isn’t the only hope for the planet that the industrialized civilizations collapse? Isn’t it our responsibility to bring that about?” – Maurice Strong

What ‘The Great Reset’ Architects Don’t Want You To Understand About Economics

It shouldn’t come as a surprise that the Vice President of the World Bank Carmen Reinhardt recently warned on October 15 that a new financial disaster looms ominously over the horizon with a vast sovereign default and a corporate debt default. Just in the past 6 months of bailouts unleashed by the blowout of the system induced by the Coronavirus lockdown, Reinhardt noted that the U.S. Federal Reserve created $3.4 Trillion out of thin air while it took 40 years to create $14 Trillion. Meanwhile panicking economists are screaming in tandem that banks across Trans Atlantic must unleash ever more hyperinflationary quantitative easing which threatens to turn our money into toilet paper while at the same time acquiescing to infinite lockdowns in response to a disease which has the fatality levels of a common flu.

The fact of the oncoming collapse itself should not be a surprise- especially when one is reminded of the $1.5 quadrillion of derivatives which has taken over a world economy which generates a mere $80 trillion/year in measurable goods and trade. These nebulous bets on insurance on bets on collateralized debts known as derivatives didn’t even exist a few decades ago, and the fact is that no matter what the Federal Reserve and European Central Bank have attempted to do to stop a new rupture of this overextended casino bubble of an economy in recent months, nothing has worked. Zero to negative percent interest rates haven’t worked, opening overnight repo loans of $100 billion/night to failing banks hasn’t worked- nor has $4.5 trillion of bailout unleashed since March 2020. No matter what these financial wizards try to do, things just keep getting worse. Rather than acknowledge what is actually happening, scapegoats have been selected to shift the blame away from reality to the point that the current crisis is actually being blamed on the Coronavirus!

This Goes Far Beyond COVID-19

Let me just state outright: That while the coronavirus may in fact be the catalyzer for the oncoming financial blowout, it is the height of stupidity to believe that it is the cause, as the seeds of the crisis goes deeper and originated much earlier than most people are prepared to admit.

To start getting at a more truthful diagnostic, it is useful to think of an economy in real (vs purely financial) terms – That is: Simply think of the economy as total system in which the body of humanity (all cultures, nations and families of the world) exist.

This co-existence is predicated on certain necessary powers of production of food, clothing, capital goods (hard and soft infrastructure), transportation and energy production. After raw materials are transformed into finished goods, these physical goods and services move from points A to B and are consumed. This is very much akin to the metabolism that maintains a living body.

Now since populations tend to grow geometrically, while resources deplete arithmetically, constant demands on new creative discoveries and technological application are also needed to meet and improve upon the needs of a growing humanity. This last factor is actually the most important because it touches on the principled element that distinguishes humanity from all other forms of life in the ecosystem which Lincoln identified wonderfully in his 1859 Discoveries and Inventions Speech:

“All creation is a mine, and every man, a miner. The whole earth, and all within it, upon it, and round about it, including himself, in his physical, moral, and intellectual nature, and his susceptibilities, are the infinitely various “leads” from which, man, from the first, was to dig out his destiny… Man is not the only animal who labors; but he is the only one who improves his workmanship. This improvement, he effects by Discoveries, and Inventions.”

In a 2016 speech by President Xi Jinping, the principles of Lincoln’s understanding were laid out by the Chinese statesman who said:

“We must consider innovation as the primary driving force of growth and the core in this whole undertaking, and human resources as the primary source to support development. We should promote innovation in theory, systems, science and technology, and culture, and make innovation the dominant theme in the work of the Party, and government, and everyday activity in society… In the 16th century, human society entered an unprecedented period of active innovation. Achievements in scientific innovation over the past five centuries have exceeded the sum total of several previous millennia. . . . Each and every scientific and industrial revolution has profoundly changed the outlook and pattern of world development… Since the second Industrial Revolution, the U.S. has maintained global hegemony because it has always been the leader and the largest beneficiary of scientific and industrial progress.”

What Lincoln and Xi laid 150 years apart are not mere hypotheses, but elementary facts of life which even the most ardent money-worshipper cannot get around.

Of course money is a perfectly useful tool to facilitate trade and get around the awkward problem of lugging bartered goods around on your back all day, but it really is just that: a supporting element to a physical process of maintenance and improvement of trans-generational existence. When fools allow themselves to loose sight of that fact and elevate money to the status of a cause of all value (simply because everyone wants it), then we find ourselves far outside the sphere of reality and in the Alice in Wonderland world of Alan Greenspan’s fantasy world where up is down, good is evil, and humans are little more than vicious monkeys.

So with that in mind, let’s take this concept and look back upon today’s crisis.

London’s ‘Big Bang’

The great “liberalization” of world commerce began with a series of waves through the 1970s, and moved into high gear with the interest rate hikes of Federal Reserve Chairman Paul Volcker in 1980-82, the effects of which both annihilated much of the small and medium sized entrepreneurs, opened the speculative gates into the “Savings and Loan” debacle and also helped cartelize mineral, food, and financial institutions into ever greater behemoths. Volcker himself described this process as the “controlled disintegration of the US economy” upon becoming Fed Chairman in 1978. The raising of interest rates to 20-21% not only shut down the life blood of much of the US economic base, but also threw the third world into greater debt slavery, as nations now had to pay usurious interest on US loans.

In 1986, the City of London announced the beginning of a new era of economic irrationalism with Margaret Thatcher’s “Big Bang” deregulation. This wave of liberalization took the world by storm as it swept aside the separation of commercial, deposit and investment banking which had been the post-world war cornerstone in ensuring that the will of private finance would never again hold more sway than the power of sovereign nation-states. For those who are confused about London’s guiding hand in this process, I encourage you to read Cynthia Chung’s impeccable essay “Sugar and Spice, and Everything Vice: The Empire’s Sin City of London”.

Greenspan and the Controlled Disintegration of the Economy

When Alan Greenspan confronted the financial crisis of October1987, markets had collapsed by 28.5% and the American economy was already suffering from a decay begun 16 years earlier when the dollar was removed from the fixed exchange rate and was “floated” into a world of speculation. This departure from the 1938-1971 Industrial growth model ushered in a new paradigm of “post-industrialism” (aka: nation stripping) under the new logic of “globalization”. This foolish decision was celebrated as the consumer-driven, “white collar society” which would no longer worry about “intangible things” like “the future”, infrastructure maintenance, or “growth”. Under this new paradigm, if something couldn’t generate a monetary profit within 3 years, it wasn’t worth doing.

Paul Volcker (Greenspan’s predecessor at the Federal Reserve) exemplified this detachment from reality when he called for the “controlled disintegration of society” in 1977, and acted accordingly by keeping interest rates above 20% for two years which destroyed small and medium agro-industrial enterprises across America (and the world). Greenspan confronted the 1987 crisis with all the gusto of a black magician, and rather than re-connect the economy to physical reality and rebuild the decaying industrial base, he chose instead to normalize “creative financial instruments” in the form of derivatives (aka: “creative financial instruments”), which quickly grew from several billion in 1988 to $2 trillion in 1992 to $70 trillion in 1999.

“Creative financial instruments” was the Orwellian name given to the new financial asset popularized by Greenspan, but otherwise known as “derivatives”. New supercomputing technologies were increasingly used in this new venture, not as the support for higher nation building practices, and space exploration programs as their NASA origins intended, but would rather become perverted to accommodate the creation of new complex formulas which could associate values to price differentials on securities and insured debts that could then be “hedged” on those very spot and futures markets made possible via the destruction of the Bretton Woods system in 1971. So while an exponentially self-generating monster was created that could end nowhere but in a meltdown, “market confidence” rallied back in force with the new flux of easy money. The physical potential to sustain human life continued to plummet.

NAFTA, the Euro and the End of History

It is no coincidence that within this period, another deadly treaty was passed called the North American Free Trade Agreement (NAFTA). With this Agreement made law, protective programs that had kept North American factories in the U.S and Canada were struck down, allowing for the export of the lifeblood of highly skilled industrial workforce to Mexico where skills were low, technologies lower, and salaries lower still. With a stripping of its productive assets, North America became increasingly reliant on exporting cheap resources and services for its means of existence. Again, the physically productive powers of society would collapse, yet monetary profits in the ephemeral “now” would skyrocket. This was replicated in Europe with the creation of the Maastricht Treaty in 1992 establishing the Euro by 1994 while the “liberalization” process of Perestroika replicated this agenda in the former Soviet Union. While some personalities gave this agenda the name “End of History” and others “the New World Order”, the effect was the same.

Universal Banking, NAFTA, Euro integration and the creation of the derivative economy in a space of just several years would induce a cartelization of finance through newly legalized mergers and acquisitions at a rate never before seen. The multitude of financial institutions that had existed in the early 1980s were absorbed into each other at great speed through the 1990s in true “survival of the fittest” fashion. No matter what level of regulation were attempted under this new structure, the degree of conflict of interest, and private political power was uncontrollable, as evidenced in the United States, by the shutdown of any attempt by Securities and Exchange Commission head Brooksley Born to fight the derivative cancer at its early stages.

When Bill Clinton repealed Glass-Steagall bank separation of commercial and investment banks as his last act in office in 1999, speculators had un-bounded access to savings and pensions which they used with relish and went to town gambling with other people’s money. This new bubble continued for a few more years until the $700 trillion derivatives time bomb found a new trigger and the subprime mortgage market nearly burned the system down. Just like in 1987, and the collapse of the Y2K bubble in 2001, the Mammon worshipping wizards in the ECB and Fed solved this crisis by creating a new system of “bailout” which continued for another decade.

The 2000-2008 Frenzy

With Glass-Steagall now removed, legitimate capital such as pension funds could be used to start a hedge to end all hedges. Billions were now poured into mortgage-backed securities (MBS), a market which had been artificially plunged to record-breaking interest rate lows of 1-2% for over a year by the US Federal Reserve making borrowing easy, and the returns on the investments into the MBSs obscene. The obscenity swelled as the values of the houses skyrocketed far beyond the real values to the tune of one hundred thousand dollar homes selling for 5-6 times that price within the span of several years. As long as no one assumed this growth was ab-normal, and the un-payable nature of the capital underlying the leveraged assets locked up in the now infamous “sub-primes” and other illegitimate debt obligations was ignored, then profits were supposed to just continue infinitely. Anyone who questioned this logic was considered a heretic by the latter-day priesthood.

The stunning “success” of securitizing housing debts immediately induced a wave of sovereign wealth funds to come into prominence applying the same model that had been used in the case of mortgage-backed securities (MBS) and collateralized debt obligations (CDO) to the debts of entire nations. The securitizing of bundled packages of sovereign debts that could then be infinitely leveraged on the de-regulated world markets would no longer be considered an act of national treason, but the key to easy money.

The Ugly Truth of Today’s Crisis

New “sub-prime” bubbles have been created in the Corporate Debt sector which has risen to over $13.8 trillion (up 16% from the year earlier). A quarter of which is considered junk, and another half graded at BB by Moodies (a step above junk).

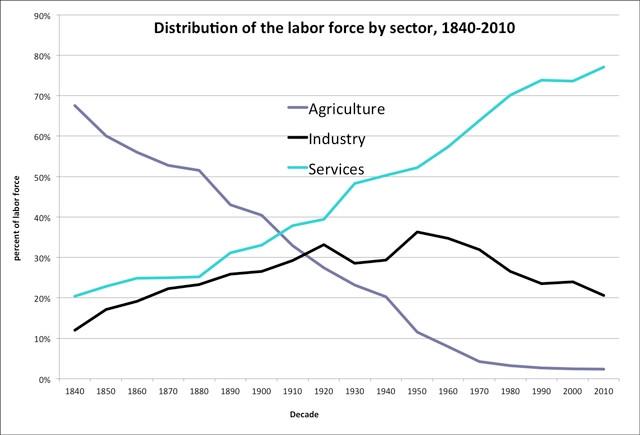

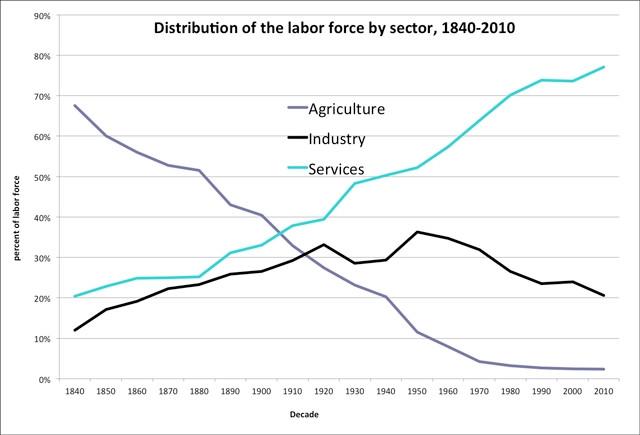

Household debt, student and auto debt has skyrocketed and since wages have not kept up with inflation causing even more unpayable debts have been incurred in desperation. Industrial jobs have collapsed consistently since 1971, and low paying service jobs have taken over like a plague.

The last report from the American Society of Civil Engineers concluded that America desperately needs to spend $4.5 trillion just to bring its decayed infrastructure up to safety levels. Roads, bridges, rail, dams, airports, schools all received near failing grades with the average age of Dams clocking in at 56 years, and many water pipes over 100 years old, and transmission/distribution lines are well over 60 years. The factories which once supplied those infrastructure needs are long outsourced, and much of the productive workforce that had that living knowledge to build a nation are retired or dead leaving a deadly generation knowledge gap in its place filled with millennials who never knew what a productive economy looked like.

American farmers have probably been the most devastated in all this with dramatic population losses across the entire farm belt of America and the average age of farmers now 60 years. It was recently reported that 82% of U.S. Agricultural family income comes from off farms, as mega cartels have taken over all aspects of farming (from equipment/supplies, packaging and the even the actual farming in between).

Combined with the controlled destruction of global food supplies internationally, COVID has ensured that strategic food chain supplies are being ripped to shreds with the UN reporting the worst food crisis in over 50 years (and that is not accounting for the oncoming blowout of the bubble economy).

Why was this permitted to happen? Well besides the obvious intention to induce “a controlled disintegration of the economy” as Volcker so coldly stated, the idea was always to create the conditions described by the late Maurice Strong (sociopath and Rothschild cut-out extraordinaire) in 1992 when he rhetorically asked:

“What if a small group of world leaders were to conclude that the principal risk to the Earth comes from the actions of the rich countries? And if the world is to survive, those rich countries would have to sign an agreement reducing their impact on the environment. Will they do it? The group’s conclusion is ‘no’. The rich countries won’t do it. They won’t change. So, in order to save the planet, the group decides: Isn’t the only hope for the planet that the industrialized civilizations collapse? Isn’t it our responsibility to bring that about?”

How do we get back to health?

Like any addict who wakes up one morning at rock bottom with the sudden terror that his death is nigh, the first step is admitting we have a problem. This means simply: acknowledging the true nature of the current economic calamity instead of trying to blame “coronavirus” or China, or some other scapegoat.

The next step is begin to act on reality instead of continuing to take heroine (a fine metaphor for the addiction to derivatives speculation).

An obvious first step to this recovery involves restoring Glass-Steagall in order to 1) break up the Too Big to Fail banks and 2) impose a standard of judging “false” value from “legitimate” value which is currently absent from the modern psycho that lost all sense of needs vs wants. This would allow nations to re-create a purge of the unpayable fictitious debt and other claims from the system while preserving whatever is tied to the real economy (whatever is directly connected to life). This process is sort of akin to cutting a cancer.

This act would look very similar to what Franklin Roosevelt did in 1933 which I outlined in my recent paper Hyperinflation, Fascism and War: How the New World Order May be Defeated Once More.

At this point nation states will have re-asserted their true authority over the pirates of private finance controlling the Trans-Atlantic financial system like would-be gods of Olympus (unbounded perverted vices and all).

It should be obvious to all that the United States must get its head out of its proverbial ass before it is too late by imposing these reforms onto the murderous sociopaths on Wall Street and London who would rather promote a “Great Reset” onto the world economy under the fog of COVD in order to control the terms of the blowout and also the rules of the new post-nation state operating system which they wish to see brought online as a (final) “solution”.

{kind=link}

{kind=link}

Pingback: CONTROLLED DEMOLITION: ‘Chaos Theory’, What The Architects Don’t Want You To Understand About Economics — RIELPOLITIK – New Human New Earth Communities

The historical pattern of civilization is an omnipotent ruler who lives well at the expense of the masses—a feudalistic society. The exceptions of this practice marks the few cultures that have made great contributions to living standards.

The pursuit of globalism is to reach the pinnacle of despotism under a guise of social advancement.

HALLELUJAH !!! It is so well written:

“It should be obvious to all that the United States must get its head out of its proverbial ass before it is too late by imposing these reforms onto the murderous sociopaths on Wall Street and London who would rather promote a “Great Reset” onto the world economy under the fog of COVD in order to control the terms of the blowout and also the rules of the new post-nation state operating system which they wish to see brought online as a (final) “solution”. End quote.

Perhaps if it was recognized the Federal Reserve is slipping $4 billion under the table daily for undetermined destinations—that legally belong to the government—we could get a hold of the problem. Ref. https://www.spartareport.com/2020/07/the-federal-reserve-for-dummies