Source – seekingalpha.com

– “…It does not take major wars to reverse globalization; domestic politics is sufficient. A very open Japan in 1633 suddenly closed itself to trade for the next two centuries, only lifting this Sakoku policy in 1866 under considerable outside pressure. Medieval China’s trading fleet never left port again after the great Yongle emperor was succeeded in 1424 by his son, whose Confucianism jarred with the idea of foreign trade….And in the early 1930s, the world fell apart into fragmented trading blocs and global trade more than halved as the US isolated itself from the world. Political u-turns on open borders can be brutally fast”:

(Investing In The Post-Truth World: Are You A Willing Guinea Pig?)

Summary

Investors seem perfectly willing to be misled these days.

What passes for the “truth” now emanates from anywhere and everywhere – even Macedonian teenagers.

Thankfully, not everyone is buying it.

My resignation

“I’ve resigned myself to it,” I once told an employer, despairing.

The “story” I was being asked to write was just that, a story. There was a video and I was essentially being pressured into spinning a narrative around that video. The narrative was, in my mind, patently absurd.

For a few fleeting moments I eyed the picture I had proudly snapped on my iPhone of my (sizeable) Christmas bonus check from the previous year. It was the largest check I’d ever seen let alone the largest check that ever had my name on the “pay to the order of” line. “Fair enough,” my boss said, accepting the fact that although I wouldn’t be accepting his narrative, I would nevertheless write the story so that I could continue accepting outsized cash Christmas presents hand delivered by FedEx.

As it turns out, I hadn’t “resigned myself to it.” Instead, I “resigned myself from it” – that is, I quit a few days later.

“There are no such things as facts”

I’ve been called a lot of things in my time; most of the disparaging labels are accurate. One that isn’t is “angry liberal.” The (somewhat sad) truth is that I live a rather solitary existence. To be perfectly honest, who inhabits the White House has very little effect on my life (far less of an effect, I imagine, than it has on the average American’s life).

What’s irked me about the current state of affairs however is that, as I explored in great detail early Friday, we’re actually witnessing an outright breakdown of politics as we know it. And part of this breakdown stems from our descent into what the FT has appropriately called the “post-truth” world.

Now let’s get to markets. What’s particularly frightening is that people are throwing money at this new reality as though it somehow represents progress when the slightest appeal to common sense reveals something altogether different. Consider the following from the FT:

Throughout the year, facts were elastic concepts.

In 2016, the world woke up to “fake news”, sponsored by political activists but also increasingly by state actors and their surrogates. Scottie Nell Hughes, a Trump supporter and CNN commentator, explained: “So one thing that’s been interesting this entire campaign season to watch, is that people that say facts are facts – they’re not really facts. Everybody has a way – it’s kind of like looking at ratings, or looking at a glass of half-full water. Everybody has a way of interpreting them to be the truth or not truth. There’s no such thing, unfortunately, anymore as facts.” Welcome to the world of post-truth politics.

“Welcome,” indeed. Actually Scottie there are “such things as facts,” and while we may not ever get to soak them up in their purest incarnation, we can get closer to them or farther away from them and that proximity in many cases depends on our own willingness to be misled.

In the personal account delineated above, I found that I was simply unwilling to deliberately mislead readers even if they were willing to be misled.

“Giving something back”

What we’re seeing with the Dow (NYSEARCA:DIA) approaching 20,000 and with analysts revising their 2017 earnings estimates higher to account for an as yet completely amorphous fiscal stimulus plan, is that investors are perfectly willing to be misled. As is the American electorate. I won’t venture too far into an analysis of the presidential campaign here (this is an investment website after all), but suffice to say that there are very real questions about the president elect’s sincerity on the campaign trail and also about the deluge of “news” items that flooded the internet in the lead-up to his election.

In short, it now appears that at least some consumers of “news” were less than discerning when it came to choosing their sources. And I don’t mean in a kind of “watch out for CNN’s liberal bias” or “beware of Fox’s conservative bent” type of way. Here are some excerpts from another FT piece, out Friday:

It was once known as “Tito’s Veles” in honour of the former Yugoslav leader who praised the gaily coloured porcelain tea sets its factories produced. But the small Macedonian riverside town of 44,000 is now better known for its wildly successful pro-Trump fake news websites.

More than a hundred US politics sites are run from Veles, where a handful of entrepreneurial Macedonian teenagers – apparently unconnected to American rightwing elements or alleged Russian operatives – produce hoax articles attracting millions of clicks and shares.

The emergence of a fake news industry in this unlikely spot in the Balkan hinterland may even have tipped the electoral balance in Donald Trump’s favour.

“No one can be sure, but it’s nice to think we could have changed the course of American history,” said Slavcho Chadiev, the town’s mayor, of the websites credited by some with helping to elect Donald Trump as US president. “Some think we should now be called ‘Trump’s Veles’,” he joked.

The hoax news creators, who decided to set up online after the success of local health websites, still make most of their money from Trump-related content. But elections next year in France and Germany offer a fresh opportunity.

A statement from one creator’s Google AdSense account showed income of more than €7,500 in November alone – no small feat in a country where the average monthly salary is about €350. “If I make €100,000 this year, I’ll pay €10,000 in taxes – that will pay for two of my teachers’ salaries for a whole year,” said one teenager, in an interview given while he skipped history class. “So, I feel like I’m giving something back.”

Ah, yes. Much like I was “giving something back” by buying tens of thousands of dollars worth of furniture and electronics with my Christmas bonus checks. I suppose I was “paying the salaries” of the Havertys and Best Buy employees of the world.

Investing in the post-truth world

But teenagers in the Balkans aren’t the only ones capitalizing off the shifting political landscape. So too are US investors who have watched equities march triumphantly higher into the new year.

Projections for 2017 don’t look so shabby either. Goldman sees the S&P (NYSEARCA:SPY) hitting 2,400 by mid-year, Deutsche Bank sees 2,350 by the end of the year and 2,500 in 2018, while Barclays is going with a year-end target of 2,400 – just to give you a few examples.

For the time being, no one seems to be concerned about the high degree of uncertainty surrounding politics in the US or about the geopolitical turbulence that very likely lies ahead for Europe, the Mid-East, and China in the year ahead.

Even the Fed is buying the story. FOMC participants were more hawkish than expected this week with regard to the outlook for rate hikes. Why? Partly because they’re buying the story about fiscal stimulus meaningfully boosting the US economy and they don’t want to find themselves “behind the curve” in the event Trump makes good on his promises.

And the biggest risk to markets is…

Having said all of that, Barclays is out Friday with its latest study of 885 global investors and what they found was that despite the short-term optimism, not everyone is buying the story when it comes to assessing “longer-term implications.”

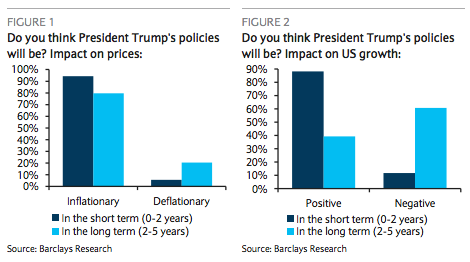

Specifically, investors overwhelmingly (or perhaps “bigly” is the better term) think that over a 2-5 year period, Trump’s policies will have a decidedly negative impact on growth.

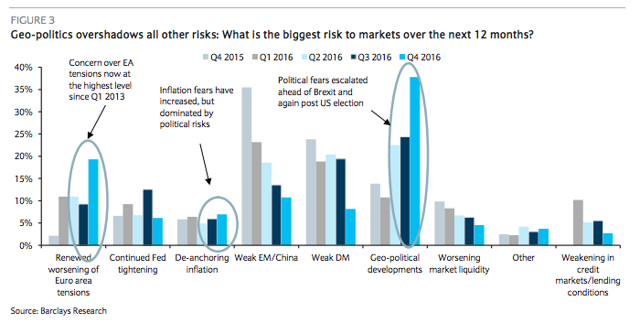

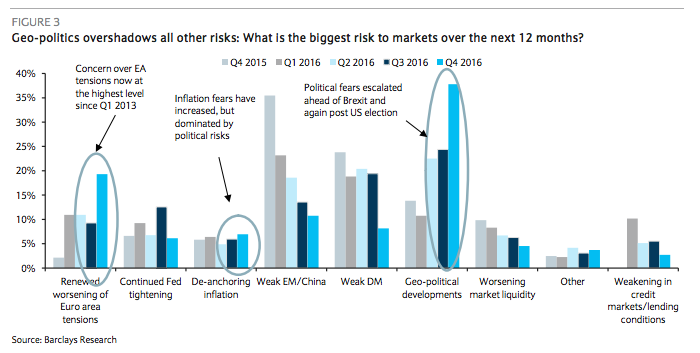

Further, investors agree with my contention that geopolitics is by far the biggest risk to markets over the next 12 months. They also expressed deep consternation about elections in France and Germany, something I also discussed earlier today in the piece cited above. Here’s Barclays:

The latest survey highlights significant shifts in the economic and financial outlook in the wake of the US election. Little is known about the shape of policy over the coming year, but the initial assessment appears to be that, in the near term, policies are likely to provide a strong boost for US growth, inflation and US equities.

Investors are, however, more sceptical with regards to the longer-term effect of Trump’s policies. While more than 80% of investors expect policies to be inflationary over the next five years, the positive boost to growth is expected to be short lived. The majority of investors fear that the growth outlook will be negative beyond the two-year time frame.

Survey respondents have become increasingly concerned about the potential market effect of geopolitical risks next year, and are now more focused on the risk of a renewed revival in euro area tensions. Investors are more pessimistic with regards to the spillover effect from European politics, where the outlooks for growth and risk assets are considered to be negative for Europe.

Political developments have dominated investors’ thinking throughout the year, a theme that is set to continue as we head into 2017. Geopolitical concerns were again voted as the biggest risk for markets over the next 12 months (Figure 3).

Investors are now also far more concerned about a renewed revival in euro area tensions, which has doubled to almost 20% and is now considered the second-biggest threat to markets. As well as uncertainty surrounding the elections in France, Germany and the Netherlands next year, the Italian referendum is likely to have influenced the results.70% of investors responded after the referendum results were known. When asked how European political forces would affect markets over the next year, over half of investors considered the effect to be negative for growth and the outlook for risk assets. Just a third on the other hand believed that there was no clear effect.

Maybe these folks just haven’t read enough articles penned by Macedonian teenagers.

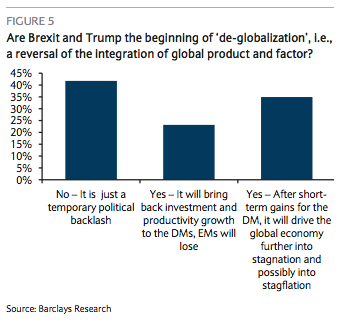

Additionally, 60% of those surveyed said Brexit and Trump’s election have likely started us down the road to deglobalization – something else I’ve expressed quite a bit of concern over:

Investors are, however, more sceptical with regards to the longer-term effect of the rise in populism. When asked if Brexit and Trump were the start of a broader “deglobalisation” process, 60% believe that yes, this was the start of a longer-term trend. Within this group, just 25% believed this would bring investment and productivity gains back to DMs from EMs, while 35% believed that the outcome would be more detrimental, leading to economic stagnation and possibly stagflation at an economic level. 41% viewed this as a short-term phenomena and part of a temporary political backlash.

Speaking of deglobalization

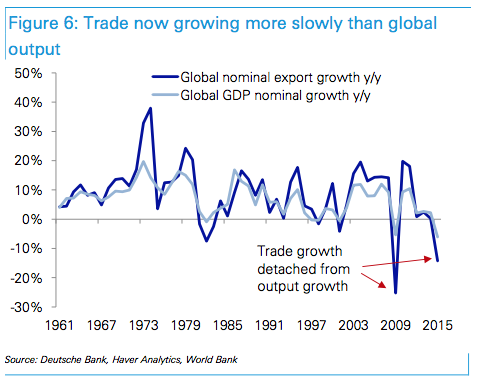

It’s a bad idea. See here’s the thing, we’re already headed down a dark road here. Global trade growth has now fallen behind the already anemic pace of global output:

(Chart: Deutsche Bank)

Here’s a bit of perspective from Deutsche Bank:

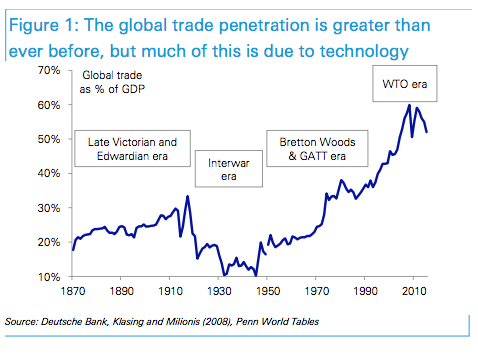

We define globalization as the rising free movement of goods, capital and people. In the post-war period, cross-border flows in all three have increased rapidly. The value of trade has risen from 17% to over 50% of global GDP since 1960 (Figure 1).

It does not take major wars to reverse globalization; domestic politics is sufficient. A very open Japan in 1633 suddenly closed itself to trade for the next two centuries, only lifting this Sakoku policy in 1866 under considerable outside pressure. Medieval China’s trading fleet never left port again after the great Yongle emperor was succeeded in 1424 by his son, whose Confucianism jarred with the idea of foreign trade.2 And in the early 1930s, the world fell apart into fragmented trading blocs and global trade more than halved as the US isolated itself from the world. Political u-turns on open borders can be brutally fast.

Marx was wrong: politics still dominates economics. And like a long pendulum it swings between laissez-faire and protectionism. The pendulum may be swinging back against globalization. Donald Trump’s election victory poses an existential threat to NAFTA and a future TPP agreement, and negotiations with Europe over TTIP have been put on permanent hold amid opposition from both sides of the Atlantic. Moreover, if Trump fails in his plans to renegotiate some key tariffs under the GATT agreement, he could even use his executive power to exit the WTO without requiring congressional approval.

In the UK, the historic decision to exit the European Union may be motivated by opposition to the free movement of people. But it also implies a willingness to sacrifice free trade and capital mobility as well.

So protectionism is back en vogue on the commanding heights of global politics. But it has shown in the nitty-gritty data for several years. World exports as a percent of GDP have peaked and have been on a steady, slow decline over the last two years.

A political shift could not come at a worse time, seeing as there has already been a structural slowdown in global trade growth relative to output growth.

Needless to say, the ramifications of all of that (e.g. a worsening USD funding crunch, reduced FDI, etc) are decisively negative – but that’s a longer discussion that’s probably best left for another time.

Fantastic stories and where to find them

Early on Friday I called this whole thing a “postmodern experiment in anti-politics” – like “populism on steroids.”

In the short-term the Guinea pigs in this experiment have enjoyed six straight weeks of higher stock prices (+8% since the election). The long-run outlook is far less sanguine, something Barclays’ survey results suggest at least some investors are starting to realize.

My advice: be careful about which stories you pick to serve as the backbone of your investment thesis. Increasingly, some of these stories aren’t based on anything that even approximates the truth. Believe me I know, I used to write them.

http://seekingalpha.com/article/4031131-investing-post-truth-world-willing-guinea-pig