Source – davidstockmanscontracorner.com

– “…To the contrary, honest free markets would actually sell the stock of corporate strip-miners, not encourage them to hit the buyback lever again and again, as do the Fed-subsidized gamblers in the fast money lanes”:

(The Fed’s Third Mandate And The Destruction Of Honest Finance, Part 1 – by David Stockman)

California Rep. Edward Royce had the temerity yesterday to ask Janet Yellen whether the Fed was propping up stock prices. Imagine that!

In fact, he hit the nail on the head when he characterized the Fed’s unrelenting intrusion in financial markets and constant dithering on rate normalization as a “third pillar”, and one found nowhere in its statutory authorities:

ROYCE: I’m worried that the Federal Reserve has created a third pillar of monetary policy, that of a stable and rising stock market. And I say that because then-Chairman Bernanke, when he appeared here, stated repeatedly that, “the goal of QE was to increase asset prices like the stock market to create a wealth effect.” That seems as though that was goal. It would stand to reason then that in deciding to raise rates and reduce the Fed’s QE balance sheet standing at a still record $4.5 trillion, one would have to be prepared to accept the opposite result, a declining stock market and a slight deflation of the asset bubble that QE created. Yet, every time in the past three years when there has been a hint of raising rates and the stock market has declined accordingly, the Fed has cited stock market volatility as one of the reasons to stay the course and hold rates at zero. So indeed, the Fed has backed away so many times from rate normalization that – and I think this is a conceptual problem here that the market now expects stock market volatility to diminish the odds of a rate increase. So Madame Chair, is having a stable and rising stock market a third pillar or the Federal Reserve’s monetary policy if I go back to what I originally heard Ben Bernanke articulate?

Yellen’s reply is a risible insult to the intelligence of anyone who can fog a mirror. The sum and substance of what the Fed does these days is wealth effects pumping via the Greenspan/Bernanke/Yellen Put, but that did not stop our duplicitous school marm from denying the obvious:

YELLEN: It is not a third pillar of monetary policy. We do not target the level of stock prices. That is not an appropriate thing for us to do.

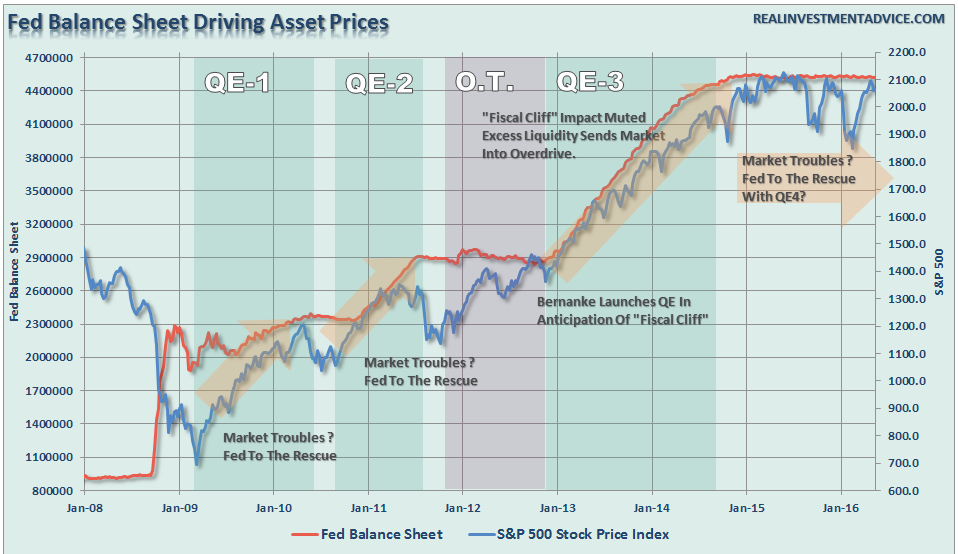

There you have the essence of the extreme danger embedded in today’s incendiary casinos. Yellen has no trouble denying the patently obvious because she does not credit what is in plain sight. If the chart below is a “coincidence”, then its truly time to don our tinfoil hats.

In fact, to the denizens of the Eccles Building reality is what the Fed’s woebegone Keynesian model tells them it should be. At the moment it is apparently saying that the bathtub of full-employment GDP is filling nicely. Or as Yellen put it in her dupe-athon on Capitol Hill this week,

‘The U.S. economy is doing well. My expectation is that the U.S. economy will continue to grow.’

Accordingly, they do not have a clue why the stock market, which they purportedly do not target, has been grinding exactly sideways for 600 days since the end of QE3 in late 2014. Nor do they recognize that its periodic lunges southward have been reversed only by another punt on interest rate normalization.

Apparently, that’s because it is not in the “model”. Indeed, what is actually in the model is statistical noise emitting from a 50-year old time warp of a closed economy that hardly existed then, and not at all now.

So the Fed’s cowardly “choke” in March was actually worthy of the disdainful epithet that Donald Trump hurtled at Senator Rubio and then some.

How could the US economy be “doing well”? Yellen blathered that phrase less than 90 days after having determined just the opposite.

Namely, that by historic standards and all prior economic learning what was an ultra-emergency economic bailout rate at 38 basis points needed to be prolonged into what is now month 90 on the zero bound.

The truth is, the Fed is stranded there, and it will continue to dither and split hairs until the on-coming recession is undeniable, and the third great bubble of this century comes crashing down in a monumental spasm of panic in the casino.

This is the inevitable outcome because the Fed’s actual “wealth effects” policy is essentially a monetary time bomb. Its fatal flaw is the presumption that by falsifying and inflating financial asset prices in order to induce households and businesses to spend and invest, respectively, that the real main street economy will eventually grow into these blatant over-valuations.

Call it the Fed’s version of the Laffer Curve: Inflate financial asset prices to a fare-thee-well, and profits will grow their way back to sensible and sustainable capitalization rates.

To the contrary, the ridiculous mispricing of the stock market this late in the business cycle—–where the S&P 500 closed today at 24.2X reported LTM earnings—-is proof that the wealth effects doctrine is completely bogus. As Congressman Royce rightly observes above, “it would stand to reason” that the Fed should have expected that an eventual normalization of rates would result in a “declining stock market”.

But you only need to peruse what the Fed’s big thinkers have said about macro-economic stimulus via the wealth effects doctrine and its obvious that Rep. Royce’s logically obvious proposition was never contemplated.

Instead, as described by Bernanke himself in the passage below, wealth effects is just another variation of mechanical Keynesian pump-priming. Rising financial asset wealth would induce households to spend, which would cause higher utilization of slack labor and business capacity. That, in turn, would generate more income and profits and then more spending and investing still, world without end.

At some point along the way, presumably, rising business profits from this virtuous Keynesian chain would permit companies to earn their way back into their Fed inflated stock prices. As Bernanke said after launching QE1,

This approach eased financial conditions in the past and, so far, looks to be effective again. Stock prices rose and long-term interest rates fell when investors began to anticipate the most recent action. Easier financial conditions will promote economic growth. For example, lower mortgage rates will make housing more affordable and allow more homeowners to refinance. Lower corporate bond rates will encourage investment. And higher stock prices will boost consumer wealth and help increase confidence, which can also spur spending.”

When you think about it, the above passage is downright goofy unless you do really believe in “trickle down” growth of wages, profits and GDP.

Then again, what if Leroy don’t want the ball?

That is, if the US economy is at Peak Debt and its economic borders are wide open, what happens when a stock market winner allocates part of his gain to consumption spending (PCE), such as on a new Porsche SUV, and part to fixed asset (FA) investment, such as on some rental housing properties?

Obviously, the added PCE dead ends; it does not mobilize domestic output, wages and then more spending and the Keynesian virtuous circle. Instead, it adds to the trade deficit (negative GDP) and to Germany’s current account and national income.

As for the FA investment in a rental property, all things being equal it will bid up the price of the existing rental stock. By contrast, new construction is caused by rising apartment occupancy rates, which is mainly a function of main street wage and salary gains, not wealth effects.

In essence, therefore, the wealth effects gain in this example would simply represent a transfer of inflated asset values from the stock market to the rental property market if the original stock appreciation were realized. And if it was simply used as collateral for borrowing from Goldman’s private wealth department, it would amount to a leveraged speculation and further inflation of aggregate asset values.

Beyond that, grant Bernanke and his wealth effects comrades their due, and assume that lower mortgage rates do cause incremental demand for residential housing units and that some are actually built. But if mortgage debt is priced off the 10-year treasury note, do they really expect that rates will stay at today’s 170 basis points until the end of time?

If rates ever normalize, and eventually they must or the monetary system will blow-up, then the same rate suppression that Bernanke says “will lower mortgage rates (and) will make housing more affordable and allow more homeowners to refinance” will cause the opposite effect down the road.

Or even before that, it will contribute to a speculative housing bubble and an eventual crash when the dumb money hits the last offer.

Or consider Bernanke’s assurance that “lower corporate bond rates will encourage investment”.

Well, that didn’t happen in the slightest, and for the same reason. Real net non-residential fixed asset investment is still 20% below 2007 levels.

Instead, the orgy of corporate borrowing that has led to a 2X growth in US corporate bonds outstanding—-from $3.5 trillion to $7 trillion since the financial crisis——was cycled back into the secondary market for existing assets via financial engineering. So Fed policy led to asset inflation, not investment and output growth, and in the worst possible manner.

To wit, stock buybacks and rampant M&A deal-making have strip-mined equity from corporate balance sheets, thereby impairing the long-run efficiency and growth capacity of American business.

Perhaps not coincidentally, just released data shows that during the last 12 months, the S&P 500 companies finally spent more on share repurchases than they did prior to the last bubble crash in 2007:

During the March 2015 to March 2016 period, U.S. companies spent a record $589.4 billion in share repurchases, according to figures released Wednesday by S&P Dow Jones Indices. That eclipsed the previous record of $589.1 billion set during the market peak in 2007.

Accordingly, since the time in 2010 when Bernanke described the beneficent impacts of the wealth effects doctrine, US companies have spent upwards of $6 trillion on stock buybacks and cash M&A deals. While the resulting share s shrinkage helped to levitate the stock market averages mightily, the national economy gained next to nothing.

Folks, these wild M&A sprees do not generate economic efficiency and added wealth due to a purported “market for corporate control”.

That would happen in an textbook free market, but we do not have one. Just consider the counterfactual.

Abolish the corporate income tax and create a level playing field between debt and equity. Eliminate the Fed’s massive intrusion in the stock and bond markets and let price discovery work its magic. Get the Fed out of pegging the money market rate at zero and thereby force hedge fund speculators to absorb the true cost of carry and the true costs of downside hedging insurance.

Under those conditions, the casino would revert back to functioning as an honest capital market. And with an honest allocation of capital, the efficiency and productivity of the US business economy would improve dramatically.

But there would not be $1 trillion of M&A deals per year—–not even close.

And no C-suite would long remain occupied by the current crop of gamblers who are recklessly leveraging corporate balance sheets to fund financial engineering gambits and quick hit gains to their stock option accounts.

To the contrary, honest free markets would actually sell the stock of corporate strip-miners, not encourage them to hit the buyback lever again and again, as do the Fed-subsidized gamblers in the fast money lanes.

At the end of the day, the correct pricing of money and capital assets is the sine qua non of true capitalist prosperity. The Fed’s wealth effects doctrine, by contrast, is based on the deliberate, systematic and sustain falsification of these crucial prices.

No wonder economic growth is grinding to a halt in America and no wonder that the flyover zone victims of the Fed’s lunacy in their tens of million are rallying to the “were not winning any more” campaign of Donald Trump.

They aren’t, as we shall explore further in Part 2.

http://davidstockmanscontracorner.com/the-feds-third-mandate-and-the-destruction-of-honest-finance/